Table of contents

- Introduction

- Project Summary

- Data Collection and Metadata

- Data preparation

- Exploratory data analysis

- Model Selection

- Hyperparameter tuning of the XGBoost model

- Data preparation for CV

- Helper functions for CV

- Dividing the hyperparameters into orthogonal groups

- Gridsearch for parameter group 1

- Acceptance threshold in the context of bias-variance trade-off

- Gridsearch for parameter group 2

- Gridsearch for parameter group 3

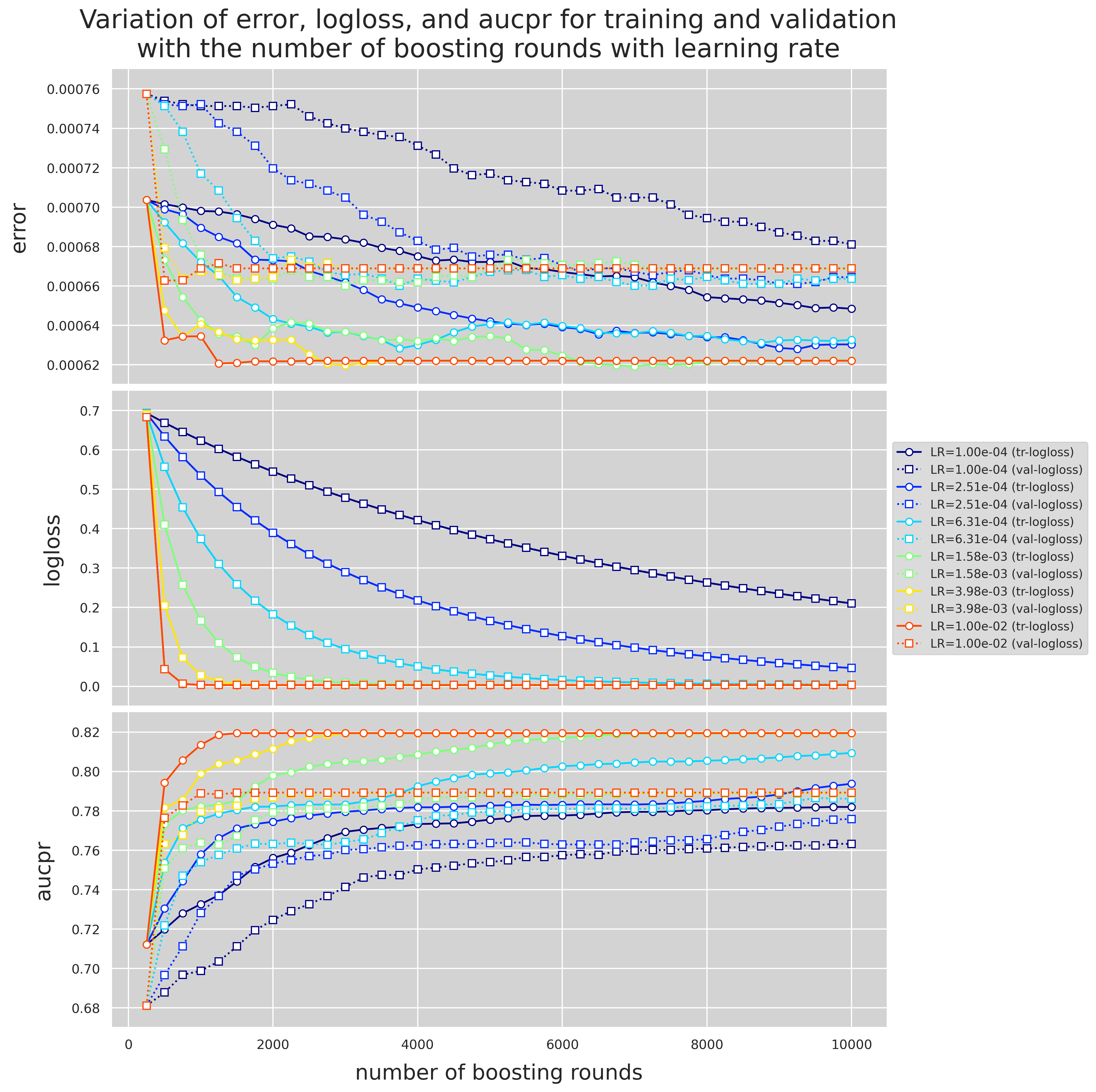

- Evolution of

eval_metricswith the number of boosting rounds andlearning_rate - Variation of

loglossandPR-AUCforgamma=3and different values ofalpha - Gridsearch for parameter group 4

- Important note regarding overfitting and the acceptance threshold

- Variation of

loglossandPR-AUCforscale_pos_weight=[1,5,20,100,1000] - Gridsearch for parameter group 5

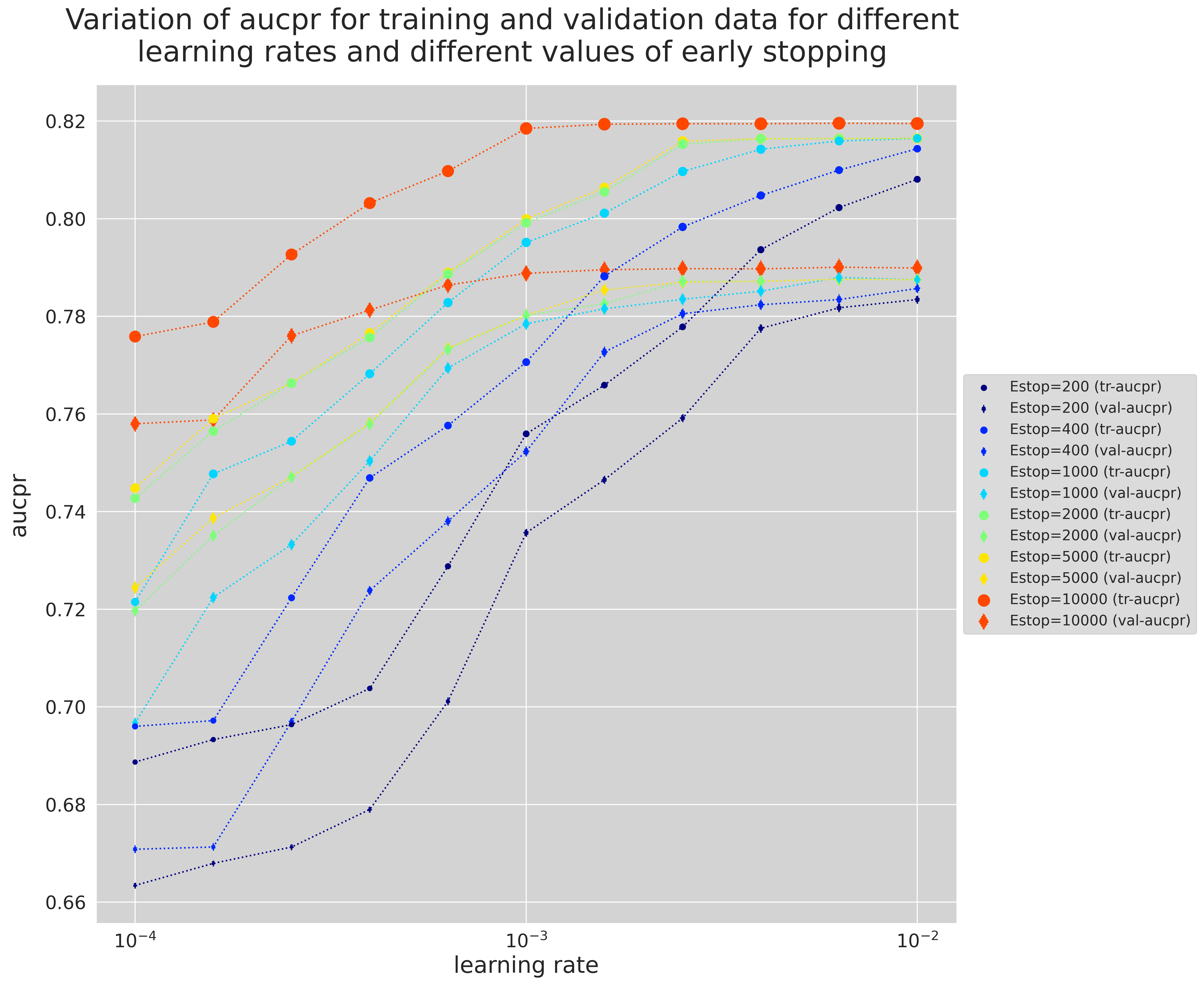

- How Early Stopping influences the optimal

learning_rate - Variation of

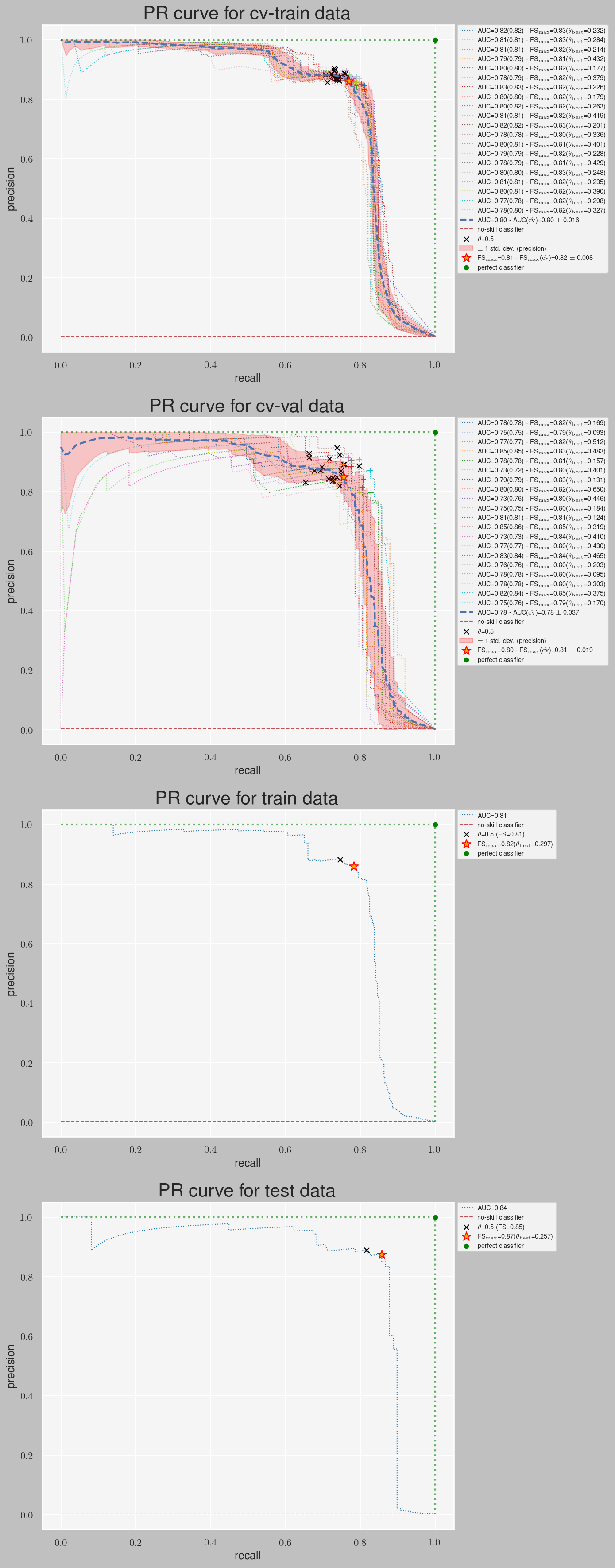

loglossandPR-AUCforalpha=0.001and different values ofgamma - Plotting the PR curves and finding the best threshold for the winner model

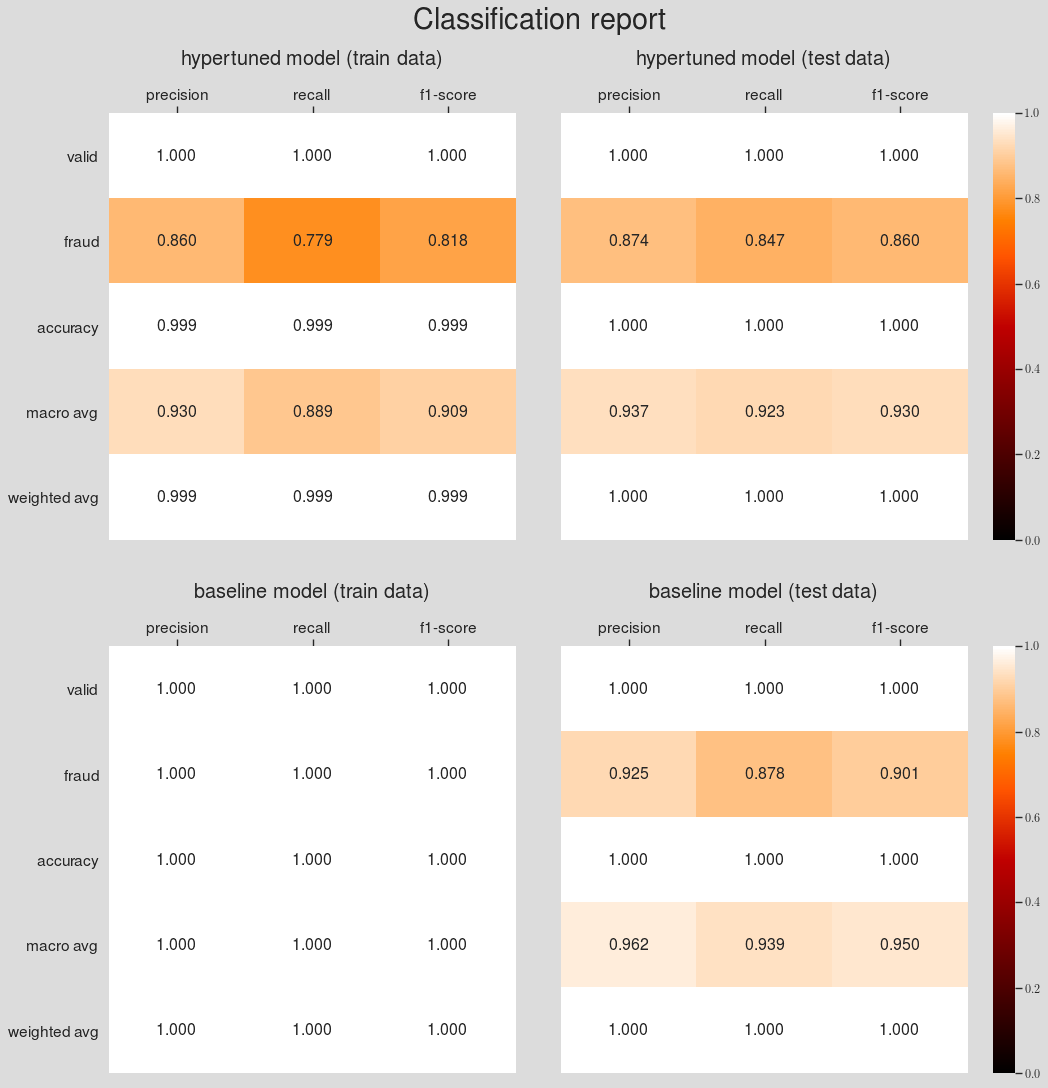

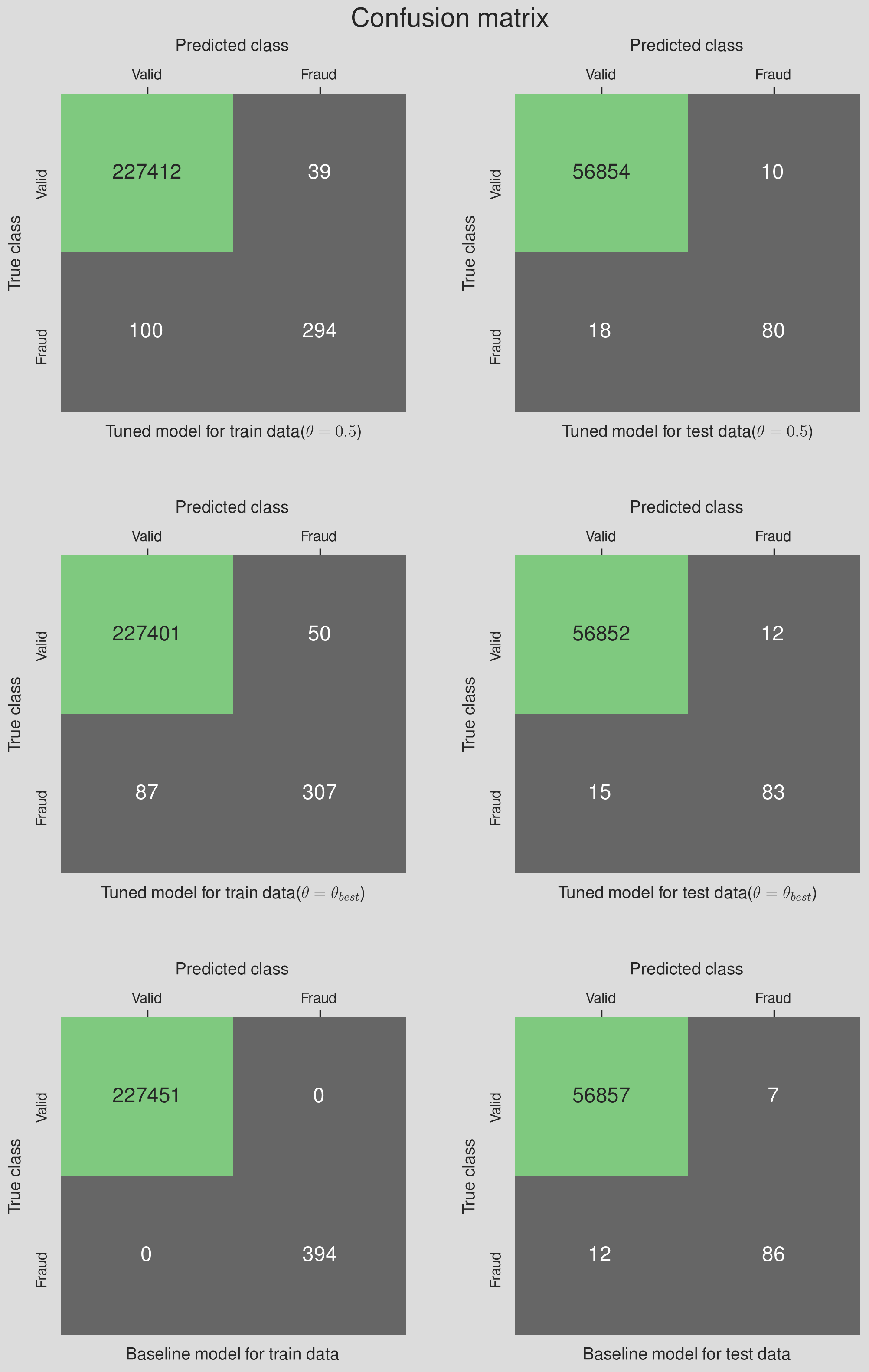

- Comparison with the baseline model

- Summary and Conclusion

- Data collection and metadata

- Data preparation

- Model selection

- Choosing the right performance metric

- Train and evaluate the models

- Comparing the model performances to find the winner model

- Hypertuning the winner model's parameters

- Comparing the winner model with the baseline model

- Models for rare-event classification

- SMOTE

- Autoencoders

- Train and evaluate the models

- Compare the model performances and find the winner model

- Make predictions

- Conclusion

- The dataset contains transactions made by credit cards in September 2013 by European cardholders.

- The dataset presents transactions that occurred in two days, where we have 492 fraud transactions among 284,807 transactions.

- The dataset is extremely imbalanced with the positive class (frauds) account for only 0.172% of all transactions.

- The dataset contains only numerical input variables which are the result of a PCA transformation.

- Due to confidentiality, the original features and more background information about the data is not provided.

- The dataset has 30 features, $\{V_1, V_2, ... V_{28}\}$ from PCA and two features which have not been transformed with PCA that are Time and Amount.

- Time shows the time elapsed (in seconds) between each transaction and the first transaction in the dataset and Amount is the transaction amount.

- Finally,Class is the response variable and it takes value 1 in case of fraud and 0 otherwise.

Introduction

Credit card fraud comes in different forms; phishing, skimming and identity theft to name a few. This project focuses on developing a supervised machine learning model that will provide the best results in revealing and preventing fraudulent transactions. Part 1 of the project compares the accuracy of different machine learning models in classifying the credit card transaction data into valid and fraud transactions.

Project Summary

Part 1: Find the best predictive model among the common ML algorithms

Part 2: Compare the accuracy of the winner of Part 1 with other algorithms that are specialized for rare-event analysis

Part 1

Data Collection and Metadata

About this data set:| Category | Type | Method | |

|---|---|---|---|

| 1 | Supervised Learning | Classification | Logistic Regression (LR) |

| 2 | Support Vector Machines (SVM) | ||

| 3 | K-Nearest Neighbours (KNN) | ||

| 4 | Naive Bayes (NB) | ||

| 5 | Artificial Neural Networks (ANN) | ||

| 6 | Random Forests (RF) | ||

| 7 | Decision Trees (DT) | ||

| 8 | XGBoost (XGB) |

Data preparation

Loading the libraries

import warnings

import matplotlib

import numpy as np

import pandas as pd

import seaborn as sns

from collections import Counter

import matplotlib.pyplot as plt

from matplotlib import cm as cm

warnings.filterwarnings('ignore')

from IPython.display import Image

from matplotlib import rc, rcParams

from IPython.core.display import HTML

matplotlib.rcParams['font.family'] = 'serif'

rc('font',**{'family':'serif','serif':['Times']})

rc('text', usetex=False)

rc('text.latex', preamble=r'\usepackage{underscore}')

pd.set_option('display.float_format', lambda x: '%.2f' % x)

sns.set(rc={"figure.dpi":100})

sns.set_style('white')Loading data

df = pd.read_csv("creditcard.csv")df.head()| Time | V1 | V2 | V3 | V4 | V5 | V6 | V7 | V8 | V9 | ... | V21 | V22 | V23 | V24 | V25 | V26 | V27 | V28 | Amount | Class | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 0 | 0.00 | -1.36 | -0.07 | 2.54 | 1.38 | -0.34 | 0.46 | 0.24 | 0.10 | 0.36 | ... | -0.02 | 0.28 | -0.11 | 0.07 | 0.13 | -0.19 | 0.13 | -0.02 | 149.62 | 0 |

| 1 | 0.00 | 1.19 | 0.27 | 0.17 | 0.45 | 0.06 | -0.08 | -0.08 | 0.09 | -0.26 | ... | -0.23 | -0.64 | 0.10 | -0.34 | 0.17 | 0.13 | -0.01 | 0.01 | 2.69 | 0 |

| 2 | 1.00 | -1.36 | -1.34 | 1.77 | 0.38 | -0.50 | 1.80 | 0.79 | 0.25 | -1.51 | ... | 0.25 | 0.77 | 0.91 | -0.69 | -0.33 | -0.14 | -0.06 | -0.06 | 378.66 | 0 |

| 3 | 1.00 | -0.97 | -0.19 | 1.79 | -0.86 | -0.01 | 1.25 | 0.24 | 0.38 | -1.39 | ... | -0.11 | 0.01 | -0.19 | -1.18 | 0.65 | -0.22 | 0.06 | 0.06 | 123.50 | 0 |

| 4 | 2.00 | -1.16 | 0.88 | 1.55 | 0.40 | -0.41 | 0.10 | 0.59 | -0.27 | 0.82 | ... | -0.01 | 0.80 | -0.14 | 0.14 | -0.21 | 0.50 | 0.22 | 0.22 | 69.99 | 0 |

5 rows × 31 columns

df.columnsIndex(['Time', 'V1', 'V2', 'V3', 'V4', 'V5', 'V6', 'V7', 'V8', 'V9', 'V10',

'V11', 'V12', 'V13', 'V14', 'V15', 'V16', 'V17', 'V18', 'V19', 'V20',

'V21', 'V22', 'V23', 'V24', 'V25', 'V26', 'V27', 'V28', 'Amount',

'Class'],

dtype='object')

counter = Counter(df['Class'])

print(f'Class distribution of the response variable: {counter}')

print(f'Minority class corresponds to {100*counter[1]/(counter[0]+counter[1]):.3f}% of the data')Class distribution of the response variable: Counter({0: 284315, 1: 492})

Minority class corresponds to 0.173% of the data

df.describe()| Time | V1 | V2 | V3 | V4 | V5 | V6 | V7 | V8 | V9 | ... | V21 | V22 | V23 | V24 | V25 | V26 | V27 | V28 | Amount | Class | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| count | 284807.00 | 284807.00 | 284807.00 | 284807.00 | 284807.00 | 284807.00 | 284807.00 | 284807.00 | 284807.00 | 284807.00 | ... | 284807.00 | 284807.00 | 284807.00 | 284807.00 | 284807.00 | 284807.00 | 284807.00 | 284807.00 | 284807.00 | 284807.00 |

| mean | 94813.86 | 0.00 | 0.00 | -0.00 | 0.00 | 0.00 | 0.00 | -0.00 | 0.00 | -0.00 | ... | 0.00 | -0.00 | 0.00 | 0.00 | 0.00 | 0.00 | -0.00 | -0.00 | 88.35 | 0.00 |

| std | 47488.15 | 1.96 | 1.65 | 1.52 | 1.42 | 1.38 | 1.33 | 1.24 | 1.19 | 1.10 | ... | 0.73 | 0.73 | 0.62 | 0.61 | 0.52 | 0.48 | 0.40 | 0.33 | 250.12 | 0.04 |

| min | 0.00 | -56.41 | -72.72 | -48.33 | -5.68 | -113.74 | -26.16 | -43.56 | -73.22 | -13.43 | ... | -34.83 | -10.93 | -44.81 | -2.84 | -10.30 | -2.60 | -22.57 | -15.43 | 0.00 | 0.00 |

| 25% | 54201.50 | -0.92 | -0.60 | -0.89 | -0.85 | -0.69 | -0.77 | -0.55 | -0.21 | -0.64 | ... | -0.23 | -0.54 | -0.16 | -0.35 | -0.32 | -0.33 | -0.07 | -0.05 | 5.60 | 0.00 |

| 50% | 84692.00 | 0.02 | 0.07 | 0.18 | -0.02 | -0.05 | -0.27 | 0.04 | 0.02 | -0.05 | ... | -0.03 | 0.01 | -0.01 | 0.04 | 0.02 | -0.05 | 0.00 | 0.01 | 22.00 | 0.00 |

| 75% | 139320.50 | 1.32 | 0.80 | 1.03 | 0.74 | 0.61 | 0.40 | 0.57 | 0.33 | 0.60 | ... | 0.19 | 0.53 | 0.15 | 0.44 | 0.35 | 0.24 | 0.09 | 0.08 | 77.16 | 0.00 |

| max | 172792.00 | 2.45 | 22.06 | 9.38 | 16.88 | 34.80 | 73.30 | 120.59 | 20.01 | 15.59 | ... | 27.20 | 10.50 | 22.53 | 4.58 | 7.52 | 3.52 | 31.61 | 33.85 | 25691.16 | 1.00 |

8 rows × 31 columns

Normalizing the features

I use Re-scaling (min-max normalization) to normalize the features. Re-scaling transforms all the numerical features to the range $[-1,\,1]$

$$ \text{min-max normalization: }x \rightarrow -1 + \frac{2(x-min(x))}{max(x)-min(x)} $$df.iloc[:,:30] = -1 + (df.iloc[:,:30] - df.iloc[:,:30].min())*2 / (df.iloc[:,:30].max() - df.iloc[:,:30].min())df.describe()| Time | V1 | V2 | V3 | V4 | V5 | V6 | V7 | V8 | V9 | ... | V21 | V22 | V23 | V24 | V25 | V26 | V27 | V28 | Amount | Class | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| count | 284807.00 | 284807.00 | 284807.00 | 284807.00 | 284807.00 | 284807.00 | 284807.00 | 284807.00 | 284807.00 | 284807.00 | ... | 284807.00 | 284807.00 | 284807.00 | 284807.00 | 284807.00 | 284807.00 | 284807.00 | 284807.00 | 284807.00 | 284807.00 |

| mean | 0.10 | 0.92 | 0.53 | 0.67 | -0.50 | 0.53 | -0.47 | -0.47 | 0.57 | -0.07 | ... | 0.12 | 0.02 | 0.33 | -0.24 | 0.16 | -0.15 | -0.17 | -0.37 | -0.99 | 0.00 |

| std | 0.55 | 0.07 | 0.03 | 0.05 | 0.13 | 0.02 | 0.03 | 0.02 | 0.03 | 0.08 | ... | 0.02 | 0.07 | 0.02 | 0.16 | 0.06 | 0.16 | 0.01 | 0.01 | 0.02 | 0.04 |

| min | -1.00 | -1.00 | -1.00 | -1.00 | -1.00 | -1.00 | -1.00 | -1.00 | -1.00 | -1.00 | ... | -1.00 | -1.00 | -1.00 | -1.00 | -1.00 | -1.00 | -1.00 | -1.00 | -1.00 | 0.00 |

| 25% | -0.37 | 0.89 | 0.52 | 0.64 | -0.57 | 0.52 | -0.49 | -0.48 | 0.57 | -0.12 | ... | 0.12 | -0.03 | 0.33 | -0.33 | 0.12 | -0.26 | -0.17 | -0.38 | -1.00 | 0.00 |

| 50% | -0.02 | 0.92 | 0.54 | 0.68 | -0.50 | 0.53 | -0.48 | -0.47 | 0.57 | -0.08 | ... | 0.12 | 0.02 | 0.33 | -0.22 | 0.16 | -0.17 | -0.17 | -0.37 | -1.00 | 0.00 |

| 75% | 0.61 | 0.96 | 0.55 | 0.71 | -0.43 | 0.54 | -0.47 | -0.46 | 0.58 | -0.03 | ... | 0.13 | 0.07 | 0.34 | -0.12 | 0.20 | -0.07 | -0.16 | -0.37 | -0.99 | 0.00 |

| max | 1.00 | 1.00 | 1.00 | 1.00 | 1.00 | 1.00 | 1.00 | 1.00 | 1.00 | 1.00 | ... | 1.00 | 1.00 | 1.00 | 1.00 | 1.00 | 1.00 | 1.00 | 1.00 | 1.00 | 1.00 |

8 rows × 31 columns

Exploratory data analysis

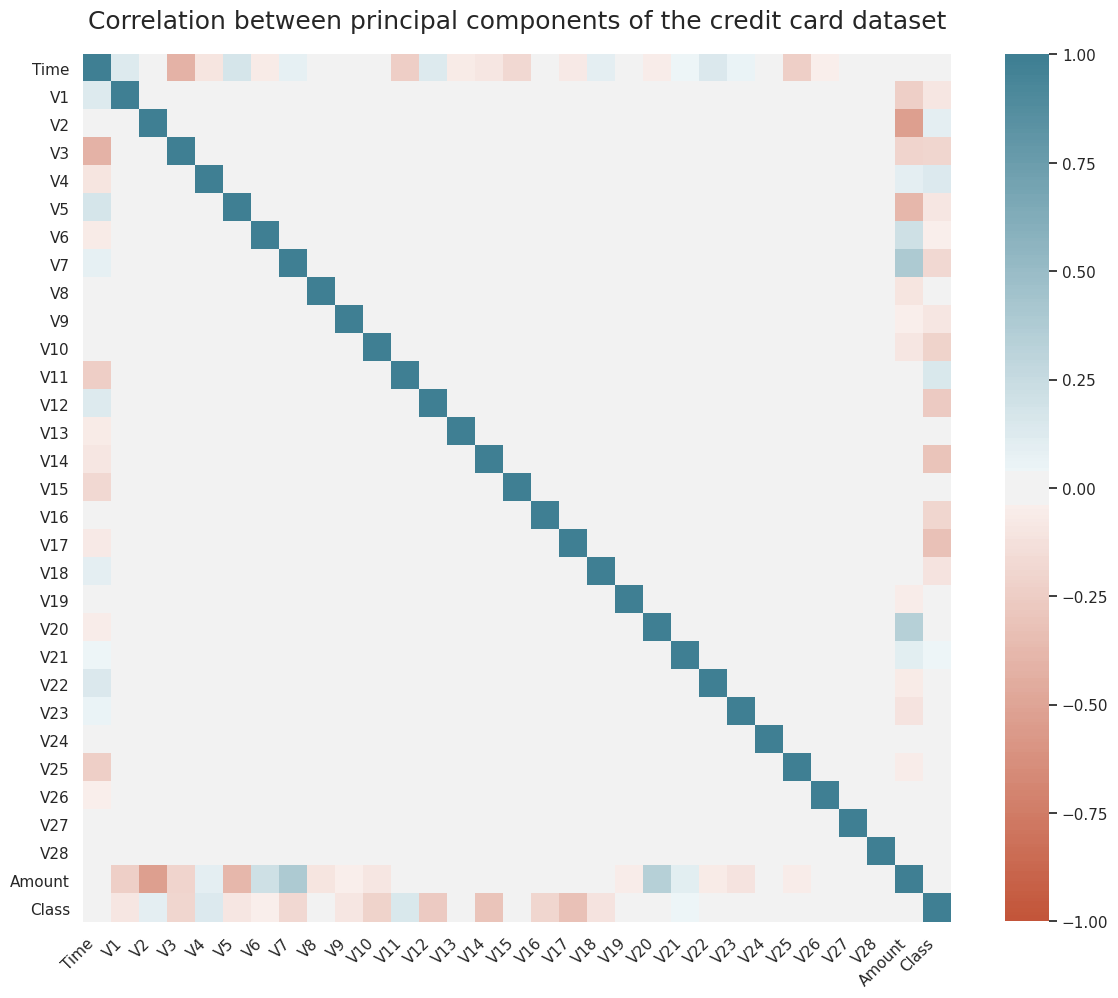

Correlation plot

fig, ax = plt.subplots(1, 1, figsize=(14,14))

corr = df.corr()

ax_ = sns.heatmap(

corr,

vmin=-1, vmax=1, center=0,

cmap=sns.diverging_palette(20, 220, n=200),

square=True,

ax=ax,

cbar_kws={'shrink': 0.82}

)

ax_.set_xticklabels(

ax.get_xticklabels(),

rotation=45,

horizontalalignment='right'

)

ax.set_title('Correlation between principal components of the credit card dataset', fontsize=18, y=1.02);

As we can see in Figure 1, most of the data features are not correlated. This is because before publishing, most of the features have been transformed using Principal Component Analysis (PCA). The importance of these features, however, could be assessed using the RandomForestClassifier.feature_importances_ of sklearn.ensemble which requires training a classification tree on the data or SelectKbest method from sklearn.feature_selection for a general model.

Feature importance

from sklearn.ensemble import RandomForestClassifier

from sklearn.feature_selection import SelectKBest

from sklearn.feature_selection import f_classif

def get_feature_importance_Kbest(X, y, feature_names, n_features_to_plot=30):

kbest = SelectKBest(score_func=f_classif, k=n_features_to_plot)

fit = kbest.fit(X, y)

feature_ids_sorted = np.argsort(fit.scores_)[::-1]

features_sorted_by_importance = np.array(feature_names)[feature_ids_sorted]

try:

feature_importance_array = np.vstack((

features_sorted_by_importance[:n_features_to_plot],

np.array(sorted(fit.scores_)[::-1][:n_features_to_plot])

)).T

except:

feature_importance_array = np.vstack((

features_sorted_by_importance[:],

np.array(sorted(fit.scores_)[::-1][:])

)).T

feature_importance_data = pd.DataFrame(feature_importance_array, columns=['feature', 'score'])

feature_importance_data['score'] = feature_importance_data['score'].astype(float)

return feature_importance_data

# Using RF feature_importances_

def get_feature_importance_RF(X, y, feature_names, n_features_to_plot=30):

RF = RandomForestClassifier(random_state=0)

RF.fit(X, y)

importances_RF = RF.feature_importances_

feature_ids_sorted = np.argsort(importances_RF)[::-1]

features_sorted_by_importance = np.array(feature_names)[feature_ids_sorted]

try:

feature_importance_array = np.vstack((

features_sorted_by_importance[:n_features_to_plot],

np.array(sorted(importances_RF)[::-1][:n_features_to_plot])

)).T

except:

feature_importance_array = np.vstack((

features_sorted_by_importance[:],

np.array(sorted(importances_RF)[::-1][:])

)).T

feature_importance_data = pd.DataFrame(feature_importance_array, columns=['feature', 'score'])

feature_importance_data['score'] = feature_importance_data['score'].astype(float)

return feature_importance_data

# Features and response variable

X = df.iloc[:,:30].values

y = df.iloc[:,30].values

feature_names = list(df.columns.values[:30])

# Using KBest

importances_KBest = get_feature_importance_Kbest(X, y, feature_names)

# Using RF

importances_RF = get_feature_importance_RF(X, y, feature_names)pd.concat([importances_RF,importances_KBest],axis=1)| RF | KBest | |||

|---|---|---|---|---|

| feature | score | feature | score | |

| 0 | V14 | 0.14 | V17 | 33979.17 |

| 1 | V17 | 0.14 | V14 | 28695.55 |

| 2 | V12 | 0.13 | V12 | 20749.82 |

| 3 | V10 | 0.09 | V10 | 14057.98 |

| 4 | V16 | 0.08 | V16 | 11443.35 |

| 5 | V11 | 0.06 | V3 | 11014.51 |

| 6 | V9 | 0.04 | V7 | 10349.61 |

| 7 | V18 | 0.03 | V11 | 6999.36 |

| 8 | V7 | 0.02 | V4 | 5163.83 |

| 9 | V4 | 0.02 | V18 | 3584.38 |

| 10 | V26 | 0.02 | V1 | 2955.67 |

| 11 | V21 | 0.02 | V9 | 2746.60 |

| 12 | V1 | 0.01 | V5 | 2592.36 |

| 13 | V6 | 0.01 | V2 | 2393.40 |

| 14 | V3 | 0.01 | V6 | 543.51 |

| 15 | V8 | 0.01 | V21 | 465.92 |

| 16 | Time | 0.01 | V19 | 344.99 |

| 17 | V5 | 0.01 | V20 | 115.00 |

| 18 | V2 | 0.01 | V8 | 112.55 |

| 19 | V20 | 0.01 | V27 | 88.05 |

| 20 | V19 | 0.01 | Time | 43.25 |

| 21 | V27 | 0.01 | V28 | 25.90 |

| 22 | V22 | 0.01 | V24 | 14.85 |

| 23 | Amount | 0.01 | Amount | 9.03 |

| 24 | V13 | 0.01 | V13 | 5.95 |

| 25 | V15 | 0.01 | V26 | 5.65 |

| 26 | V24 | 0.01 | V15 | 5.08 |

| 27 | V28 | 0.01 | V25 | 3.12 |

| 28 | V25 | 0.01 | V23 | 2.05 |

| 29 | V23 | 0.01 | V22 | 0.18 |

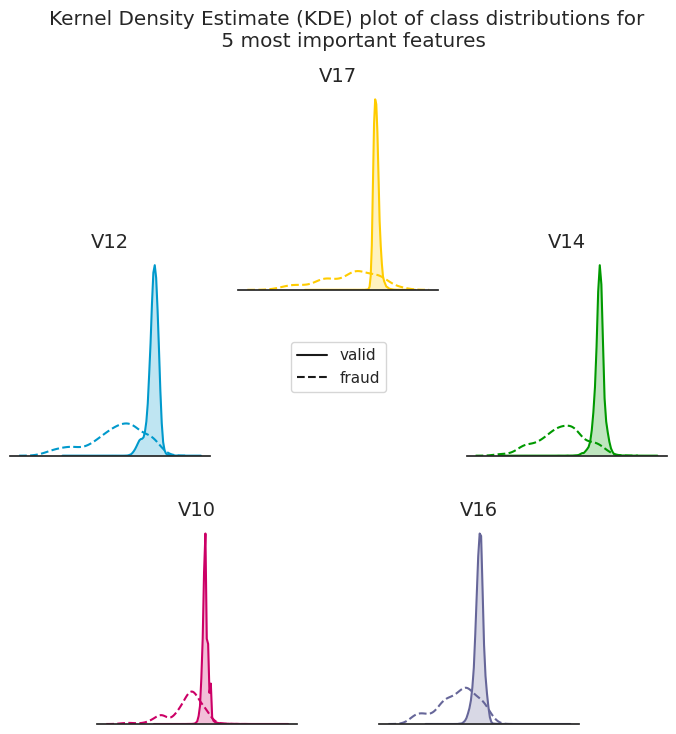

Note that the two methods rank the features similarly in terms of importance.

Class distributions for the 5 most important fatures

cols = ["#009900", "#ffcc00", "#0099cc", "#cc0066", "#666699"]

fig = plt.figure(figsize=(8,8), dpi=100)

important_features = ['V14','V17','V12','V10','V16']

theta=2*np.pi/5

offset = np.pi/2 - theta

radius = 0.3

pentagon_vertices = [[0.5+radius*(np.cos(x*theta+offset)),

0.5+radius*(np.sin(x*theta+offset))]

for x in range(5)]

for i, col in enumerate(important_features):

tmp_ax =fig.add_axes([pentagon_vertices[i][0],

pentagon_vertices[i][1],

.25,

.25])

sns.kdeplot(df[df['Class']==0][col], shade=True, color=cols[i], ax=tmp_ax)

sns.kdeplot(df[df['Class']==1][col], shade=False, color=cols[i], ax=tmp_ax, linestyle="--")

tmp_ax.set_xticklabels([])

tmp_ax.set_yticklabels([])

tmp_ax.set_title(important_features[i], fontsize=14)

if i==len(important_features)-1:

leg = tmp_ax.get_legend()

leg.legendHandles[0].set_color('k')

leg.legendHandles[1].set_color('k')

plt.legend([], [], frameon=False)

fig.legend(leg.legendHandles, ['valid','fraud'], loc='center')

sns.despine(left=True)

plt.suptitle('Kernel Density Estimate (KDE) plot of class distributions for \n 5 most important features', x=0.64, y=1.15);

Model Selection

This part explains the model selection process. We use the sklearn implementation of the candidate models except for the XGBoost classifier where we use the xgboost library.

Notes regarding the model selection process

-

Due to the extreme class imbalance in the dataset, we take advantage of the

sklearn's Stratified K-Folds cross-validator (StratifiedKFold) to ensure that the observations are distributed with a similar class ratio $\bigg(\dfrac{\text{positive class count}}{\text{negative class count}}\bigg)$ across the folds. -

We choose

scoring='average_precision'as the model evaluation criteria. Ideally we'd want to use Precision-Recall Area Under Curve (PR-AUC) as the criteria but since it is not provided bysklearn, we useaverage_precision(AP) which summarizes a precision-recall curve as the weighted mean of precisions achieved at each threshold, with the increase in recall from the previous threshold used as the weight:

$$

\text{AP} = \sum_n (R_n - R_{n-1}) P_n,

$$

where $P_n$ and $R_n$ are the precision and recall, respectively, at the $n$-th threshold [ref].

# A whole host of Scikit-learn models

from sklearn.svm import SVC

from sklearn.naive_bayes import GaussianNB

from sklearn.ensemble import GradientBoostingClassifier

from sklearn.linear_model import LogisticRegression

from sklearn.neighbors import KNeighborsClassifier

from sklearn.tree import DecisionTreeClassifier

from xgboost import XGBClassifier

from sklearn.ensemble import RandomForestClassifier

from sklearn.pipeline import make_pipeline

from sklearn.model_selection import train_test_split

from sklearn.model_selection import cross_val_score

from sklearn.model_selection import StratifiedKFold

import time

# We use StratifiedKFold to guarantee similar distribution in train and test data

# We set the train:test ratio to 4:1 - The train set will ultimately be split

# into train and validation sets itself, with the same ratio! See below

# X

# ___________/\___________

# / \

# x_1, x_2, x_3, ... , x_n

# X_train X_test

# _______/\_______ __/\__

# / \ / \

# X_test will be unseen until the very last step!

# X_train

# _______/\_______

# / \

# ||

# ||

# \/

#

# X_tr X_val

# ____/\____ _/\_

# / \/ \

num_splits = 5

skf = StratifiedKFold(n_splits=num_splits, random_state=1, shuffle=True)

# Features and response variable

X = df.iloc[:,:30].values

y = df.iloc[:,30].values

X_train, X_test, y_train, y_test = train_test_split(X, y, test_size=0.2, random_state=1, stratify=y)

model_dict = {'CT':[DecisionTreeClassifier()],

'GB':[GradientBoostingClassifier()],

'KNN':[KNeighborsClassifier()],

'LR':[LogisticRegression()],

'NB':[GaussianNB()],

'RF':[RandomForestClassifier()],

'SVC':[SVC()],

'XGB':[XGBClassifier()]}Comparing the model performances to find the winner model

for model_name, model in model_dict.items():

# train the model

t_start = time.time()

cv_results = cross_val_score(model[0],

X_train,

y_train,

cv=skf,

scoring='average_precision',

verbose=10,

n_jobs=-1)

# save the results

calc_time = time.time() - t_start

model_dict[model_name].append(cv_results)

model_dict[model_name].append(calc_time)

print(("{0} model gives an AP of {1:.2f}% with a standard deviation "

"{2:.2f} (took {3:.1f} seconds)").format(model_name,

100*cv_results.mean(),

100*cv_results.std(),

calc_time)

) [Parallel(n_jobs=-1)]: Using backend LokyBackend with 24 concurrent workers.

[Parallel(n_jobs=-1)]: Done 2 out of 5 | elapsed: 15.6s remaining: 23.4s

[Parallel(n_jobs=-1)]: Done 3 out of 5 | elapsed: 15.8s remaining: 10.5s

[Parallel(n_jobs=-1)]: Done 5 out of 5 | elapsed: 16.9s remaining: 0.0s

[Parallel(n_jobs=-1)]: Done 5 out of 5 | elapsed: 16.9s finished

[Parallel(n_jobs=-1)]: Using backend LokyBackend with 24 concurrent workers.

CT model gives an AP of 53.17% with a standard deviation 3.44 (took 17.1 seconds)

[Parallel(n_jobs=-1)]: Done 2 out of 5 | elapsed: 4.6min remaining: 6.9min

[Parallel(n_jobs=-1)]: Done 3 out of 5 | elapsed: 4.6min remaining: 3.1min

[Parallel(n_jobs=-1)]: Done 5 out of 5 | elapsed: 4.7min remaining: 0.0s

[Parallel(n_jobs=-1)]: Done 5 out of 5 | elapsed: 4.7min finished

[Parallel(n_jobs=-1)]: Using backend LokyBackend with 24 concurrent workers.

GB model gives an AP of 59.87% with a standard deviation 4.48 (took 279.6 seconds)

[Parallel(n_jobs=-1)]: Done 2 out of 5 | elapsed: 1.8min remaining: 2.7min

[Parallel(n_jobs=-1)]: Done 3 out of 5 | elapsed: 2.0min remaining: 1.3min

KNN model gives an AP of 78.70% with a standard deviation 3.31 (took 131.1 seconds)

[Parallel(n_jobs=-1)]: Done 5 out of 5 | elapsed: 2.2min remaining: 0.0s

[Parallel(n_jobs=-1)]: Done 5 out of 5 | elapsed: 2.2min finished

[Parallel(n_jobs=-1)]: Using backend LokyBackend with 24 concurrent workers.

[Parallel(n_jobs=-1)]: Done 2 out of 5 | elapsed: 2.9s remaining: 4.3s

[Parallel(n_jobs=-1)]: Done 3 out of 5 | elapsed: 2.9s remaining: 1.9s

[Parallel(n_jobs=-1)]: Done 5 out of 5 | elapsed: 3.1s remaining: 0.0s

[Parallel(n_jobs=-1)]: Done 5 out of 5 | elapsed: 3.1s finished

[Parallel(n_jobs=-1)]: Using backend LokyBackend with 24 concurrent workers.

LR model gives an AP of 72.42% with a standard deviation 2.56 (took 3.3 seconds)

[Parallel(n_jobs=-1)]: Done 2 out of 5 | elapsed: 0.5s remaining: 0.8s

[Parallel(n_jobs=-1)]: Done 3 out of 5 | elapsed: 0.5s remaining: 0.4s

[Parallel(n_jobs=-1)]: Done 5 out of 5 | elapsed: 0.5s remaining: 0.0s

[Parallel(n_jobs=-1)]: Done 5 out of 5 | elapsed: 0.5s finished

[Parallel(n_jobs=-1)]: Using backend LokyBackend with 24 concurrent workers.

NB model gives an AP of 8.54% with a standard deviation 0.50 (took 0.7 seconds)

[Parallel(n_jobs=-1)]: Done 2 out of 5 | elapsed: 2.7min remaining: 4.0min

[Parallel(n_jobs=-1)]: Done 3 out of 5 | elapsed: 2.7min remaining: 1.8min

[Parallel(n_jobs=-1)]: Done 5 out of 5 | elapsed: 3.0min remaining: 0.0s

[Parallel(n_jobs=-1)]: Done 5 out of 5 | elapsed: 3.0min finished

[Parallel(n_jobs=-1)]: Using backend LokyBackend with 24 concurrent workers.

RF model gives an AP of 84.02% with a standard deviation 3.00 (took 180.4 seconds)

[Parallel(n_jobs=-1)]: Done 2 out of 5 | elapsed: 10.4s remaining: 15.6s

[Parallel(n_jobs=-1)]: Done 3 out of 5 | elapsed: 10.5s remaining: 7.0s

[Parallel(n_jobs=-1)]: Done 5 out of 5 | elapsed: 10.7s remaining: 0.0s

[Parallel(n_jobs=-1)]: Done 5 out of 5 | elapsed: 10.7s finished

[Parallel(n_jobs=-1)]: Using backend LokyBackend with 24 concurrent workers.

SVC model gives an AP of 75.22% with a standard deviation 3.54 (took 10.8 seconds)

[Parallel(n_jobs=-1)]: Done 2 out of 5 | elapsed: 1.6min remaining: 2.4min

[Parallel(n_jobs=-1)]: Done 3 out of 5 | elapsed: 1.6min remaining: 1.1min

XGB model gives an AP of 84.89% with a standard deviation 2.92 (took 98.1 seconds)

[Parallel(n_jobs=-1)]: Done 5 out of 5 | elapsed: 1.6min remaining: 0.0s

[Parallel(n_jobs=-1)]: Done 5 out of 5 | elapsed: 1.6min finished

XGB and RF outperform the other algorithms with XGB being slightly more accurate than the random forest classifier so as we said previously, we choose XGB as the winner. In the next part, we will go through the process of tuning the model.

Hyperparameter tuning of the XGBoost model

In this part, we'd like to find the set of model parameters that work best on our credit card fraud detection problem. How can we configure the model so that we get the best model performance for the dataset we have and the evaluation metric that we specify?

We are aiming to achieve this while ensuring that the resulted parameters don't cause overfitting. We use XGBClassifier() with the default parameters as the baseline classifier. The following describes a summary of the steps and some important notes regarding the model parameters and cross-validation methodology:

- We split the data into training and test splits while maintaining the class ratio (exactly what we did in the model selection)

-

Model performance on the test data

(X_test, y_test)is not going to be assessed until the final model evaluation where both the baseline classifier and the tuned model are going to be tested against the unseen test data -

We use

RepeatedStratifiedKFold()which repeats theStratifiedKFold()$n_{\mathrm{repeats}}$ times ($3\leq n_{\mathrm{repeats}} \leq 10$) and outputs the model performance-metric (PR-AUC in this case) as the mean across all folds and all repeats. This improves the estimate of the mean model performance-metric with the downside of increased model-evaluation cost. We use $n_{\mathrm{repeats}}=5$ in this work. - early stopping is one way to reduce overfitting of training data. Here's a brief summary of how it works:

-

The user specifies an evaluation metric (

eval_metric) and a validation set (eval_set) to be monitored during the training process. -

The evaluation metric for the

eval_setneeds to "improve" at least once everyearly_stopping_roundsof boosting rounds so that the training continues. -

Early stopping terminates the training process when the number of boosting rounds with no improvement in evaluation-metric for the

eval_setreachesearly_stopping_rounds. -

XGBoostoffers a wide range of evaluation metrics (see here for the full list) that are either minimized (RMSE, log loss, etc.) or maximized (MAP, NDCG, AUC) during the training process. We useaucprfor this classification problem for the reasons discussed earlier. -

Normally, we would use

sklearn`sGridsearchCV()to find the hyperparameters of the model. This works great, especially if the model is a native sklearn model. Infact, most sklearn models come with their CV version, e.g.,LogisticRegressionCV(), which performs grid search over the user-defined hyperparameter dictionary. However, as we mentioned, when we try to useXGBoost's early stopping, we need to specify aneval_setto compare the evaluation-metric performance on it with that of the training data. Now if we useGridSearchCV(), ideally we would wantXGBoostto use the held-out fold as the evaluation set to determine the optimal number of boosting rounds, however, that doesn't seem to be possible when usingGridSearchCV(). One way is to use a static held-out set for XGBoost but that doesn't make sense as it defeats the purpose of cross validation. To address this issue, I defined a custom cross-validation function that for each hyperparameter-set candidate: -

For each fold, finds the optimal number of boosting rounds, the number of rounds where the

eval_metricreached its best value (best_score) for theeval_set. -

Reports the mean and standard deviation of the

eval_metric(for both training and evaluation data) and best number of rounds by averaging over the folds. -

Finally, returns the optimal combination of hyperparameters that gave the best

eval_metric. -

Note:

xgboost.best_ntree_limityou do best_nrounds = int(best_nrounds / 0.8) you consider that your validation set was 20% of your whole training data (another way of saying that you performed a 5-fold cross-validation). The rule can then be generalized as: n_folds = 5 best_nrounds = int((res.shape[0] - estop) / (1 - 1 / n_folds)) -

Because

XGBClassifier()accepts a lot of hyperparameters, it would be computationally inefficient and extremely time-consuming to iterate over the enormous number of hyperparameter combinations. What we can do instead is to divide the parameters into a few independent or weakly-interacting groups and find the best hyperparameter combination for each group. The optimal set of parameters can ultimately be determined as the union of the best hyperparameter groups. The following is the hyperparameter groups and the order that we optimize them (reference): max_depth,min_child_weightcolsample_bytree,colsample_bylevel,subsamplealpha,gammascale_pos_weightlearning_rate-

To ensure that the model hyperparameters don't cause overfitting, we save the model's

eval_metricresults for both training and validation data. At the end, we throw out the set of hyperparameters where the model exhibits a better performance for the training data than the validation data. -

Because we are using early stopping, the model throws out the optimal number of trees (

n_estimators) for each fold. For each parameter group, the best number of boosting trees is returned as the mean over the folds. -

We use a Python

dictionary,progress, to record the changes in validation and training dataeval_metric(s). This can help a lot with assessing whether the model is overfitting or not. - Our efforts to reduce overfitting are in accordance with XGBoost's Notes on Parameter Tuning.

Data preparation for CV

import xgboost as xgb

from sklearn.model_selection import RepeatedStratifiedKFold

from sklearn.model_selection import train_test_split

# load data

X = df.iloc[:,:30].values

y = df.iloc[:,30].values

all_features = list(df.columns.values[:30])

# train-test stratified split; stratify=y is used to ensure

# that the two splits have similar class distribution

X_train, X_test, y_train, y_test = train_test_split(X, y, test_size=0.2, random_state=1, stratify=y)

model = XGBClassifier(tree_method='gpu_hist',

objective='binary:logistic')

# fold parameters

num_splits = 4

num_reps = 5

rand_state = 123

rskf = RepeatedStratifiedKFold(n_splits=num_splits,

n_repeats=num_reps,

random_state=rand_state)Helper functions for CV

First, we define a function that for the given set of hyperparameters, trains the XGBClassifier() and spits out the model's mean-over-folds performance metrics.

from sklearn.metrics import average_precision_score

from datetime import datetime, timedelta

from itertools import product

from pprint import pprint

np.set_printoptions(threshold=5)

Early_Stop_Rounds = 400

Num_Boosting_Rounds = 4000

from sklearn.metrics import average_precision_score

from datetime import datetime, timedelta

from itertools import product

from pprint import pprint

import random

np.set_printoptions(threshold=5)

Early_Stop_Rounds = 400

Num_Boosting_Rounds = 4000

def cv_summary(X_data, y_data, params, feature_names, cv,

objective_func='binary:logistic',

eval_metric='aucpr',

spit_out_fold_results=False,

spit_out_summary=True,

num_boost_rounds=Num_Boosting_Rounds,

early_stop_rounds=Early_Stop_Rounds,

save_fold_preds=False):

"""

Returns cv results for a given set of parameters

"""

# number of folds

num_splits = cv.cvargs['n_splits']

# num_rounds: total number of rounds (= n_repeats*n_folds)

num_rounds = cv.get_n_splits()

# train_scores and val_scores store the mean over all repeats of

# the in-sample and held-out predictions, respectively

train_scores = np.zeros(num_rounds)

valid_scores = np.zeros(num_rounds)

best_num_estimators = np.zeros(num_rounds)

# track eval results

eval_results = []

fold_preds = {'train':[], 'eval':[]}

for i, (train_index, valid_index) in enumerate(cv.split(X_data, y_data)):

# which repeat

rep = i//num_splits + 1

# which fold

fold = i%num_splits + 1

# XGBoost train uses DMatrix

xg_train = xgb.DMatrix(X_data[train_index,:],

feature_names=feature_names,

label = y_data[train_index])

xg_valid = xgb.DMatrix(X_data[valid_index,:],

feature_names=feature_names,

label = y_data[valid_index])

# set evaluation

params['tree_method'] = 'gpu_hist'

params['objective'] = objective_func

params['eval_metric'] = eval_metric

# track eval results

progress = dict()

# train using train data

if early_stop_rounds is not None:

clf = xgb.train(params, xg_train,

num_boost_round = num_boost_rounds,

evals=[(xg_train, "train"), (xg_valid, "eval")],

early_stopping_rounds=early_stop_rounds,

evals_result=progress,

verbose_eval=False)

# for validation data we don't need to set ntree_limit because from

# XGBoost docs:

#

# fit():

#

# if early_stopping_rounds is not None:

# self.best_ntree_limit = self._Booster.best_ntree_limit

# ...

# ...

# predict():

#

# if ntree_limit is None:

# ntree_limit = getattr(self, "best_ntree_limit", 0)

y_pred_vl = clf.predict(xgb.DMatrix(X_train[valid_index,:],

feature_names=feature_names))

# for train data, we scale up the number of rounds, i.e., we consider that the

# validation set size was 1/num_splits of the training data size. Essentially

# what we report as the optimal number of boosting trees is for a data with

# the size of the training data

best_num_estimators[i] = int(clf.best_ntree_limit / (1 - 1 / num_splits))

# clf.setattr("best_ntree_limit", best_num_estimators[i])

y_pred_tr = clf.predict(xgb.DMatrix(X_train[train_index,:],

feature_names=feature_names))

else:

clf = xgb.train(params, xg_train,

num_boost_round = num_boost_rounds,

evals=[(xg_train, "train"), (xg_valid, "eval")],

verbose_eval=False,

evals_result=progress)

best_num_estimators[i] = num_boost_rounds

y_pred_tr = clf.predict(xgb.DMatrix(X_train[train_index,:],

feature_names=feature_names),

ntree_limit=0)

y_pred_vl = clf.predict(xgb.DMatrix(X_train[valid_index,:],

feature_names=feature_names),

ntree_limit=0)

train_scores[i] = average_precision_score(y_train[train_index], y_pred_tr)

valid_scores[i] = average_precision_score(y_train[valid_index], y_pred_vl)

if save_fold_preds:

fold_preds['train'].append([y_train[train_index], y_pred_tr])

fold_preds['eval'].append([y_train[valid_index], y_pred_vl])

if spit_out_fold_results:

print(f"\n Repeat {rep}, Fold {fold} -",

f"PR-AUC tr = {train_scores[i]:<.3f},",

f"PR-AUC vl = {valid_scores[i]:<.3f}",

f"(diff = {train_scores[i] - valid_scores[i]:<.4f})",

)

if early_stop_rounds is not None:

print(f" best number of boosting rounds tr = {best_num_estimators[i]:<.0f}")

eval_results.append(progress)

# End of each repeat

if spit_out_summary:

print(f"\nSummary:\n",

f"mean PR-AUC training = {np.average(train_scores):<.3f}\n",

f"mean PR-AUC validation = {np.average(valid_scores):<.3f}\n",

f"mean PR-AUC difference = {np.average(train_scores-valid_scores):<.4f}"

)

if early_stop_rounds is not None:

print(f" average number of boosting rounds tr = {np.average(best_num_estimators):<.0f}")

out = [(np.average(x), np.std(x)) for x in [train_scores, valid_scores, best_num_estimators]]

return out, eval_results, fold_preds, clf

def cv_search_params(X_data, y_data, param_dict, feature_names, cv,

objective_func='binary:logistic', eval_metric='aucpr',

spit_out_fold_results=False, spit_out_summary=True,

num_boost_rounds=Num_Boosting_Rounds,

early_stop_rounds=None, random_grid_search = False,

save_fold_preds=False,

num_random_search_candidates=10):

"""

Returns the cv_summary() for all the combinations of the given parameter dictionary

"""

search_results = []

param_values = [

x if (isinstance(x, list) or isinstance(x, type(np.linspace(1,2,2))))

else [x] for x in param_dict.values()

]

param_dict = dict(zip(tuple(param_dict.keys()), param_values))

num_search_candidates = len(list(product(*param_values)))

all_search_params = []

num_rand_search_candidates = num_random_search_candidates

random_sample_ids = random.sample(range(num_search_candidates), num_rand_search_candidates)

all_search_params = []

for i, search_params in enumerate(product(*param_values)):

current_params = dict(zip(tuple(param_dict.keys()), search_params))

all_search_params.append(current_params)

if random_grid_search:

all_search_params = list(np.array(all_search_params)[random_sample_ids])

evals = [[] for i in range(len(all_search_params))]

print(f"Grid search started at {datetime.now()}")

print(f"Total number of hyperparameter candidates = {len(evals)}")

for i, search_params in enumerate(all_search_params):

start_time = datetime.now()

current_params = search_params

print(f'\nCV {i+1} on:\n')

pprint({k: v for k, v in current_params.items() if len(param_dict[k])>1})

print('\n started!')

results, evals[i], _, _ = cv_summary(X_data, y_data,

current_params, feature_names,

cv, objective_func=objective_func,

eval_metric=eval_metric,

spit_out_fold_results=spit_out_fold_results,

spit_out_summary=spit_out_summary,

early_stop_rounds=early_stop_rounds,

num_boost_rounds=num_boost_rounds)

end_time = datetime.now()

time_taken = f"{(end_time-start_time).total_seconds():.2f}"

if len(evals)>1:

print(f'CV {i+1} ended! (took {time_taken} seconds)')

else:

print(f'CV ended! (took {time_taken} seconds)')

[(tr_avg, tr_std),

(val_avg, val_std),

(numtrees_avg, numtrees_std)] = results

search_results.append([current_params,

tr_avg, tr_std,

val_avg, val_std,

numtrees_avg, numtrees_std,

tr_avg-val_avg, time_taken])

print(f"Grid search ended at {datetime.now()}")

search_df = pd.DataFrame(search_results,

columns=['current_params', 'tr_avg', 'tr_std',

'val_avg', 'val_std', 'numtrees_avg',

'numtrees_std', 'diff', 'time_taken'])

return search_df, evalsDividing the hyperparameters into orthogonal groups

Next, we define a hyperparameter dictionary and update it with some initial parameters for the model:

cur_params = {

'max_depth': 3,

'min_child_weight': 5,

'subsample': 1,

'colsample_bytree': 1,

'colsample_bylevel': 1,

'alpha': 1,

'gamma': 1,

'scale_pos_weight': 1,

'learning_rate': 2e-3,

}We then define the parameter groups that are going to be the target of grid search:

# current xgb parameters

param_group_1 = {'max_depth': [3, 4], 'min_child_weight': [1, 10, 20, 30, 40]}

param_group_2 = {'subsample': np.linspace(0.1, 1, 5),

'colsample_bytree': np.linspace(0.1, 1, 5),

'colsample_bylevel': np.linspace(0.1, 1, 5)}

param_group_3 = {'alpha': np.logspace(-6, 3, 4), 'gamma': np.linspace(1, 9, 5)}

param_group_4 = {'scale_pos_weight': [0.5, 1, 2, 5, 10, 20, 50, 100, 500, 1000]}

param_group_5 = {'learning_rate': np.logspace(-4, -2, 11)}Gridsearch for parameter group 1: max_depth and min_child_weight

We update the cur_params before performing the hyperparameter search. Also, it's a good practice to save the grid search results to minimize the chances of data loss. We use .to_pickle() method of pandas to save the resulting DataFrame.

search_params = param_group_1

cur_params.update(search_params)

pprint(cur_params) {'alpha': 1,

'colsample_bylevel': 1,

'colsample_bytree': 1,

'gamma': 1,

'learning_rate': 0.002,

'max_depth': [3, 4],

'min_child_weight': [1, 10, 20, 30, 40],

'scale_pos_weight': 1,

'subsample': 1}

tmp_df, evals = cv_search_params(X_train, y_train, cur_params, all_features, rskf)

tmp_df.to_pickle('hyperparams_round1.pkl') Grid search on:

{'alpha': 1,

'colsample_bylevel': 1,

'colsample_bytree': 1,

'gamma': 1,

'learning_rate': 0.002,

'max_depth': [3, 4],

'min_child_weight': [1, 10, 20, 30, 40],

'scale_pos_weight': 1,

'subsample': 1}

started at 2021-06-04 12:41:46.384232

Total number of hyperparameter candidates = 10

CV 1 on:

{'max_depth': 3, 'min_child_weight': 1}

started!

Repeat 1, Fold 1 - PR-AUC tr = 0.816, PR-AUC vl = 0.752 (diff = 0.0639)

best number of boosting rounds tr = 386

Repeat 1, Fold 2 - PR-AUC tr = 0.871, PR-AUC vl = 0.813 (diff = 0.0584)

best number of boosting rounds tr = 5289

Repeat 1, Fold 3 - PR-AUC tr = 0.823, PR-AUC vl = 0.789 (diff = 0.0336)

best number of boosting rounds tr = 1209

...

Repeat 5, Fold 2 - PR-AUC tr = 0.762, PR-AUC vl = 0.739 (diff = 0.0232)

best number of boosting rounds tr = 1397

Repeat 5, Fold 3 - PR-AUC tr = 0.708, PR-AUC vl = 0.742 (diff = -0.0342)

best number of boosting rounds tr = 838

Repeat 5, Fold 4 - PR-AUC tr = 0.700, PR-AUC vl = 0.683 (diff = 0.0165)

best number of boosting rounds tr = 1110

Summary:

mean PR-AUC training = 0.728

mean PR-AUC validation = 0.718

mean PR-AUC difference = 0.0094

CV 10 ended! (took 319.31 seconds)

Grid search ended at 2021-06-04 14:17:32.954835

tmp_df| current_params | tr_avg | tr_std | val_avg | val_std | numtrees_avg | numtrees_std | diff | time_taken | |

|---|---|---|---|---|---|---|---|---|---|

| 0 | {'max_depth': 3, 'min_child_weight': 1, 'subsa... | 0.847 | 0.025 | 0.810 | 0.039 | 3163.150 | 1663.705 | 0.037 | 696.55 |

| 1 | {'max_depth': 3, 'min_child_weight': 10, 'subs... | 0.848 | 0.018 | 0.816 | 0.032 | 4030.550 | 1415.623 | 0.032 | 857.18 |

| 2 | {'max_depth': 3, 'min_child_weight': 20, 'subs... | 0.808 | 0.024 | 0.779 | 0.051 | 2194.450 | 1672.490 | 0.029 | 518.94 |

| 3 | {'max_depth': 3, 'min_child_weight': 30, 'subs... | 0.784 | 0.017 | 0.767 | 0.040 | 1859.400 | 1292.788 | 0.017 | 452.01 |

| 4 | {'max_depth': 3, 'min_child_weight': 40, 'subs... | 0.728 | 0.027 | 0.718 | 0.052 | 1168.550 | 277.548 | 0.009 | 319.31 |

| 5 | {'max_depth': 4, 'min_child_weight': 1, 'subsa... | 0.874 | 0.042 | 0.817 | 0.037 | 3179.400 | 1812.708 | 0.057 | 783.87 |

| 6 | {'max_depth': 4, 'min_child_weight': 10, 'subs... | 0.844 | 0.026 | 0.806 | 0.050 | 3240.800 | 1910.967 | 0.038 | 769.04 |

| 7 | {'max_depth': 4, 'min_child_weight': 20, 'subs... | 0.810 | 0.025 | 0.780 | 0.051 | 2319.850 | 1727.073 | 0.030 | 574.93 |

| 8 | {'max_depth': 4, 'min_child_weight': 30, 'subs... | 0.784 | 0.018 | 0.767 | 0.040 | 1858.900 | 1292.927 | 0.017 | 455.43 |

| 9 | {'max_depth': 4, 'min_child_weight': 40, 'subs... | 0.728 | 0.027 | 0.718 | 0.052 | 1168.550 | 277.548 | 0.009 | 319.31 |

We can remove the rows where the difference between the training and validation performance is significant. I take the threshold for this difference to be 2%, meaning that we disregard the parameters that cause a difference in performance $>2\%$ between training and validation sets. For the rest of this project, we will refer to this threshold as the acceptance threshold (not to be confused with the precision-recall threshold) and to this condition as the acceptance condition. This reduces the chances that the final model parameters cause overfitting. At the same time, we sort the output by val_avg which is the mean PR-AUC over the validation sets.

acceptance_threshold=0.02

cur_params = param_df[param_df['diff']<acceptance_threshold] \

.sort_values('val_avg', ascending=False)| current_params | tr_avg | tr_std | val_avg | val_std | numtrees_avg | numtrees_std | diff | time_taken | |

|---|---|---|---|---|---|---|---|---|---|

| 3 | {'max_depth': 3, 'min_child_weight': 30, 'subs... | 0.784 | 0.017 | 0.767 | 0.040 | 1859.400 | 1292.788 | 0.017 | 452.01 |

| 8 | {'max_depth': 4, 'min_child_weight': 30, 'subs... | 0.784 | 0.018 | 0.767 | 0.040 | 1858.900 | 1292.927 | 0.017 | 455.43 |

max_depth=3 and min_child_weight=30 gives a reasonable PR-AUC while ensuring that the model's performance on the test data remains close to that of the training data. Note that using max_depth=4 gives the same performance as max_depth=3 so we move forward with the latter to reduce the complexity of the model. Next, we examine the second hyperparameter group.

Acceptance threshold in the context of bias-variance trade-off

We can think of acceptance condition in the context of bias-variance trade-off.

We say a model has a high bias if it fails to use all the data in the observations. Such model relies mostly on the general information without taking into account the specifics. In contrast, we say a model has a high variance if it over-use theinformation in the data, i.e., relies too much on the specific data that is being trained on. Such model usually fails to generalize what it has learnt and reproduce its high performance when predicting the outcome for new, unseen data.

We can demonstrate this using an example relevant to our problem. The table below shows aucpr for two models I and II. When comparing the two models, model I exhibits a very high aucpr on the training data (low bias) but a significant difference in performance when tested on the test data (high variance); Model II on the other hand gives a comparatively lower aucpr on both the training and test data (high bias) but the model's performance on both datasets is quite similar (low variance)

| Model I | Model II | |||

|---|---|---|---|---|

| train | test | train | test | |

| 0.99 | 0.8 | 0.75 | 0.73 | |

| Bias | low | high | ||

| Variance | high | low | ||

high bias and high variance both lead to errors in model performance. Ideally we would want the model to have low bias (less error on training data) and low variance (less difference between the model performance between the train and testing data). Bias-variance trade-off is the sweet spot where the model performs between the errors introduced by the bias and the variance. In this project, I used acceptance condition to set a value for Bias-variance trade-off; however, depending on the business goal, one may use a totally different criteria to find the best model hyperparameters.

Gridsearch for parameter group 2: colsample_bylevel, colsample_bytree, and subsample

We update cur_params using the parameters obtained in previous step.

cur_params.update({'max_depth': 3, 'min_child_weight': 30})

search_params = param_group_2

cur_params.update(search_params)

pprint(cur_params){'alpha': 1,

'colsample_bylevel': array([0.1 , 0.325, 0.55 , 0.775, 1. ]),

'colsample_bytree': array([0.1 , 0.325, 0.55 , 0.775, 1. ]),

'gamma': 1,

'learning_rate': 0.002,

'max_depth': 3,

'min_child_weight': 30,

'scale_pos_weight': 1,

'subsample': array([0.1 , 0.325, 0.55 , 0.775, 1. ])}

tmp_df, evals = cv_search_params(X_train, y_train, cur_params, all_features, rskf) Grid search started at 2021-05-24 10:48:53.507958

Total number of hyperparameter candidates = 125

CV 1 on:

{'subsample': 0.1, 'colsample_bylevel': 0.1, 'colsample_bytree': 0.1}

started!

Summary:

mean PR-AUC training = 0.211

mean PR-AUC validation = 0.197

mean PR-AUC difference = 0.014

best number of boosting rounds = 703

CV 1 ended! (took 191.91 seconds)

...

CV 125 on:

{'subsample': 1.0, 'colsample_bylevel': 1.0, 'colsample_bytree': 1.0}

started!

Summary:

mean PR-AUC training = 0.784

mean PR-AUC validation = 0.767

mean PR-AUC difference = 0.0171

best number of boosting rounds = 1859

CV 125 ended! (took 475.21 seconds)

Grid search ended at 2021-05-24 12:27:25.227479

tmp_df[tmp_df['diff']<acceptance_threshold].sort_values('val_avg', ascending=False)| index | current_params | tr_avg | tr_std | val_avg | val_std | numtrees_avg | numtrees_std | diff | time_taken |

|---|---|---|---|---|---|---|---|---|---|

| 124 | {'max_depth': 3, 'min_child_weight': 30, 'subs... | 0.784 | 0.017 | 0.767 | 0.033 | 1859.600 | 1409.712 | 0.016 | 475.21 |

| 119 | {'max_depth': 3, 'min_child_weight': 30, 'subs... | 0.777 | 0.014 | 0.765 | 0.037 | 547.000 | 536.632 | 0.011 | 207.12 |

| 123 | {'max_depth': 3, 'min_child_weight': 30, 'subs... | 0.775 | 0.010 | 0.761 | 0.039 | 214.250 | 229.384 | 0.014 | 146.70 |

| 118 | {'max_depth': 3, 'min_child_weight': 30, 'subs... | 0.776 | 0.015 | 0.760 | 0.041 | 691.100 | 889.920 | 0.015 | 235.01 |

| 114 | {'max_depth': 3, 'min_child_weight': 30, 'subs... | 0.777 | 0.016 | 0.760 | 0.045 | 1015.400 | 1382.065 | 0.017 | 292.21 |

| ... | ... | ... | ... | ... | ... | ... | ... | ... | ... |

| 5 | {'max_depth': 3, 'min_child_weight': 30, 'subs... | 0.211 | 0.039 | 0.211 | 0.055 | 862.600 | 364.775 | -0.000 | 215.35 |

| 10 | {'max_depth': 3, 'min_child_weight': 30, 'subs... | 0.203 | 0.037 | 0.210 | 0.068 | 1018.400 | 510.480 | -0.007 | 239.26 |

| 1 | {'max_depth': 3, 'min_child_weight': 30, 'subs... | 0.211 | 0.052 | 0.197 | 0.062 | 703.450 | 378.373 | 0.014 | 191.28 |

| 2 | {'max_depth': 3, 'min_child_weight': 30, 'subs... | 0.211 | 0.052 | 0.197 | 0.062 | 703.450 | 378.373 | 0.014 | 191.46 |

| 0 | {'max_depth': 3, 'min_child_weight': 30, 'subs... | 0.211 | 0.052 | 0.197 | 0.062 | 703.450 | 378.373 | 0.014 | 191.91 |

125 rows × 9 columns

Note that all the hyperparameter candidates satisfy the acceptance condition. We can query the first 10 hyperparameters with the best average PR-AUC on the validation data using:

[list(map(tmp_df[tmp_df['diff']<acceptance_threshold] \

.sort_values('val_avg', ascending=False)['current_params'] \

.iloc[x] \

.get,

['subsample', 'colsample_bytree', 'colsample_bylevel']

)

) for x in range(10)

][[1.0, 1.0, 1.0], [1.0, 0.775, 1.0], [1.0, 1.0, 0.775], [1.0, 0.775, 0.775], [1.0, 0.55, 1.0], [1.0, 1.0, 0.325], [1.0, 1.0, 0.55], [1.0, 0.775, 0.55], [1.0, 0.55, 0.775], [0.775, 1.0, 1.0]]

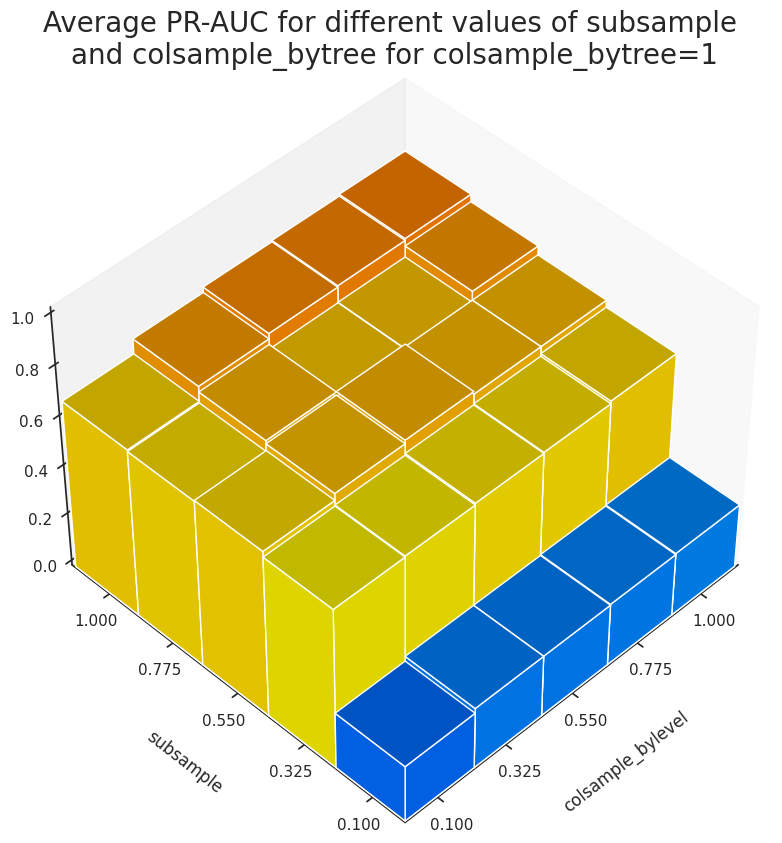

The results suggest that colsample_bylevel doesn't influenece the accuracy of the predictions. We can take a look at the evolution of PR-AUC for colsample_bylevel=1 and different values of subsample and colsample_bytree in our grid-search space.

fig = plt.figure(figsize=(10,10))

fig.tight_layout()

ax = fig.add_subplot(111, projection='3d')

ax.view_init(elev=45, azim=-135)

params = ['subsample', 'colsample_bytree', 'colsample_bylevel']

param_values = np.linspace(0.1,1,5)

indices = [x for x in range(len(tmp_df)) if tmp_df['current_params'] \

.iloc[x] \

.get('colsample_bylevel')==1]

_xx, _yy = np.meshgrid(param_values, param_values)

width = depth = 0.225

xdata, ydata = _xx.ravel()-width/2, _yy.ravel()-depth/2

zdata = tmp_df['val_avg'] \

.iloc[indices] \

.values \

.reshape(xdata.shape)

bottom = np.zeros_like(zdata)

# Get desired colormap - you can change this!

cmap = cm.get_cmap('jet')

rgba = [cmap(k) for k in zdata]

ax.bar3d(xdata, ydata, bottom, width, depth, zdata, color=rgba, zsort='max',shade=True)

ax.set_xlim([min(xdata)+0.03, max(xdata)+width])

ax.set_ylim([min(ydata)+0.03, max(ydata)+depth])

ax.set_zlim([0, 1])

ax.set_xticks(param_values)

ax.set_yticks(param_values)

plt.title("Average PR-AUC for different values of subsample \nand colsample_bytree for colsample_bytree=1", fontsize=20)

plt.ylabel("subsample", labelpad=20)

plt.xlabel("colsample_bylevel", labelpad=20)

ax.grid(False)

plt.savefig("paramgr")

plt.show()

Figure 3 shows that the variation of subsample has the most significant effect on the accuracy of the model.

Finally, we set the first row of the resulting DataFrame as the initial hyperparameter for the next round of grid search.

cur_params = tmp_df[tmp_df['diff']<acceptance_threshold] \

.sort_values('val_avg', ascending=False)['current_params'] \

.iloc[0]

pprint(cur_params){'alpha': 1,

'colsample_bylevel': 1.0,

'colsample_bytree': 1.0,

'gamma': 1,

'learning_rate': 0.002,

'max_depth': 3,

'min_child_weight': 30,

'scale_pos_weight': 1,

'subsample': 1.0}

Gridsearch for parameter group 3: alpha and gamma

cur_params.update(param_group_3)

pprint(cur_params){'alpha': array([1.e-06, 1.e-03, 1.e+00, 1.e+03]),

'colsample_bylevel': 1.0,

'colsample_bytree': 1.0,

'gamma': array([1., 3., 5., 7., 9.]),

'learning_rate': 0.002,

'max_depth': 3,

'min_child_weight': 30,

'scale_pos_weight': 1,

'subsample': 1.0}

tmp_df, evals = cv_search_params(X_train, y_train, cur_params, all_features, rskf)

tmp_df.to_pickle('hyperparams_round3.pkl')Grid search on:

{'alpha': array([1.e-06, 1.e-03, 1.e+00, 1.e+03]),

'colsample_bylevel': 1.0,

'colsample_bytree': 1.0,

'eval_metric': 'aucpr',

'gamma': array([1., 3., 5., 7., 9.]),

'learning_rate': 0.002,

'max_depth': 3,

'min_child_weight': 30,

'objective': 'binary:logistic',

'scale_pos_weight': 1.0,

'subsample': 1.0,

'tree_method': 'gpu_hist'}

started at 2021-06-07 12:26:51.336554

Total number of hyperparameter candidates = 20

CV 1 on:

{'alpha': 1e-06, 'gamma': 1.0}

started!

Summary:

mean PR-AUC training = 0.781

mean PR-AUC validation = 0.762

mean PR-AUC difference = 0.0192

average number of boosting rounds tr = 1450

CV 1 ended! (took 384.88 seconds)

CV 2 on:

{'alpha': 1e-06, 'gamma': 3.0}

started!

Summary:

mean PR-AUC training = 0.788

mean PR-AUC validation = 0.773

mean PR-AUC difference = 0.0157

average number of boosting rounds tr = 2000

CV 2 ended! (took 471.16 seconds)

CV 3 on:

{'alpha': 1e-06, 'gamma': 5.0}

started!

Summary:

mean PR-AUC training = 0.784

mean PR-AUC validation = 0.772

mean PR-AUC difference = 0.0129

average number of boosting rounds tr = 1809

CV 3 ended! (took 432.78 seconds)

CV 4 on:

{'alpha': 1e-06, 'gamma': 7.0}

started!

Summary:

mean PR-AUC training = 0.782

mean PR-AUC validation = 0.764

mean PR-AUC difference = 0.0177

average number of boosting rounds tr = 1881

CV 4 ended! (took 440.80 seconds)

CV 5 on:

{'alpha': 1e-06, 'gamma': 9.0}

started!

Summary:

mean PR-AUC training = 0.778

mean PR-AUC validation = 0.759

mean PR-AUC difference = 0.0187

average number of boosting rounds tr = 1506

CV 5 ended! (took 375.05 seconds)

CV 6 on:

{'alpha': 0.001, 'gamma': 1.0}

started!

Summary:

mean PR-AUC training = 0.782

mean PR-AUC validation = 0.763

mean PR-AUC difference = 0.0190

average number of boosting rounds tr = 1516

CV 6 ended! (took 395.33 seconds)

CV 7 on:

{'alpha': 0.001, 'gamma': 3.0}

started!

Summary:

mean PR-AUC training = 0.788

mean PR-AUC validation = 0.773

mean PR-AUC difference = 0.0158

average number of boosting rounds tr = 2023

CV 7 ended! (took 474.74 seconds)

CV 8 on:

{'alpha': 0.001, 'gamma': 5.0}

started!

Summary:

mean PR-AUC training = 0.785

mean PR-AUC validation = 0.772

mean PR-AUC difference = 0.0130

average number of boosting rounds tr = 2004

CV 8 ended! (took 463.54 seconds)

CV 9 on:

{'alpha': 0.001, 'gamma': 7.0}

started!

Summary:

mean PR-AUC training = 0.782

mean PR-AUC validation = 0.764

mean PR-AUC difference = 0.0177

average number of boosting rounds tr = 1880

CV 9 ended! (took 441.33 seconds)

CV 10 on:

{'alpha': 0.001, 'gamma': 9.0}

started!

Summary:

mean PR-AUC training = 0.778

mean PR-AUC validation = 0.759

mean PR-AUC difference = 0.0188

average number of boosting rounds tr = 1506

CV 10 ended! (took 375.77 seconds)

CV 11 on:

{'alpha': 1.0, 'gamma': 1.0}

started!

Summary:

mean PR-AUC training = 0.784

mean PR-AUC validation = 0.767

mean PR-AUC difference = 0.0171

average number of boosting rounds tr = 1859

CV 11 ended! (took 452.86 seconds)

CV 12 on:

{'alpha': 1.0, 'gamma': 3.0}

started!

Summary:

mean PR-AUC training = 0.784

mean PR-AUC validation = 0.770

mean PR-AUC difference = 0.0147

average number of boosting rounds tr = 1930

CV 12 ended! (took 457.49 seconds)

CV 13 on:

{'alpha': 1.0, 'gamma': 5.0}

started!

Summary:

mean PR-AUC training = 0.779

mean PR-AUC validation = 0.765

mean PR-AUC difference = 0.0137

average number of boosting rounds tr = 1604

CV 13 ended! (took 395.10 seconds)

CV 14 on:

{'alpha': 1.0, 'gamma': 7.0}

started!

Summary:

mean PR-AUC training = 0.780

mean PR-AUC validation = 0.761

mean PR-AUC difference = 0.0186

average number of boosting rounds tr = 1687

CV 14 ended! (took 410.15 seconds)

CV 15 on:

{'alpha': 1.0, 'gamma': 9.0}

started!

Summary:

mean PR-AUC training = 0.776

mean PR-AUC validation = 0.756

mean PR-AUC difference = 0.0197

average number of boosting rounds tr = 1556

CV 15 ended! (took 379.72 seconds)

CV 16 on:

{'alpha': 1000.0, 'gamma': 1.0}

started!

Summary:

mean PR-AUC training = 0.672

mean PR-AUC validation = 0.672

mean PR-AUC difference = -0.0001

average number of boosting rounds tr = 420

CV 16 ended! (took 168.22 seconds)

CV 17 on:

{'alpha': 1000.0, 'gamma': 3.0}

started!

Summary:

mean PR-AUC training = 0.672

mean PR-AUC validation = 0.672

mean PR-AUC difference = -0.0001

average number of boosting rounds tr = 420

CV 17 ended! (took 168.11 seconds)

CV 18 on:

{'alpha': 1000.0, 'gamma': 5.0}

started!

Summary:

mean PR-AUC training = 0.672

mean PR-AUC validation = 0.672

mean PR-AUC difference = -0.0001

average number of boosting rounds tr = 420

CV 18 ended! (took 168.26 seconds)

CV 19 on:

{'alpha': 1000.0, 'gamma': 7.0}

started!

Summary:

mean PR-AUC training = 0.672

mean PR-AUC validation = 0.672

mean PR-AUC difference = -0.0001

average number of boosting rounds tr = 420

CV 19 ended! (took 167.94 seconds)

CV 20 on:

{'alpha': 1000.0, 'gamma': 9.0}

started!

Summary:

mean PR-AUC training = 0.672

mean PR-AUC validation = 0.672

mean PR-AUC difference = -0.0001

average number of boosting rounds tr = 420

CV 20 ended! (took 168.19 seconds)

Grid search ended at 2021-06-07 14:34:06.880364

tmp_df[tmp_df['diff']<acceptance_threshold] \

.sort_values('val_avg', ascending=False) \

.head()| current_params | tr_avg | tr_std | val_avg | val_std | numtrees_avg | numtrees_std | diff | time_taken | |

|---|---|---|---|---|---|---|---|---|---|

| 1 | {'max_depth': 3, 'min_child_weight': 30, 'subs... | 0.788 | 0.017 | 0.773 | 0.033 | 1999.550 | 1415.553 | 0.016 | 471.16 |

| 6 | {'max_depth': 3, 'min_child_weight': 30, 'subs... | 0.788 | 0.017 | 0.773 | 0.033 | 2022.600 | 1409.712 | 0.016 | 474.74 |

| 7 | {'max_depth': 3, 'min_child_weight': 30, 'subs... | 0.785 | 0.018 | 0.772 | 0.035 | 2003.700 | 1534.701 | 0.013 | 463.54 |

| 2 | {'max_depth': 3, 'min_child_weight': 30, 'subs... | 0.784 | 0.017 | 0.772 | 0.034 | 1809.200 | 1205.948 | 0.013 | 432.78 |

| 11 | {'max_depth': 3, 'min_child_weight': 30, 'subs... | 0.784 | 0.018 | 0.770 | 0.036 | 1929.900 | 1284.865 | 0.015 | 457.49 |

At this point, the resulting optimal parameters achieve extremely close results in terms of the model performance metric.

[list(map(tmp_df[tmp_df['diff']<acceptance_threshold] \

.sort_values('val_avg', ascending=False)['current_params'] \

.iloc[x] \

.get,

['alpha', 'gamma']

)

) for x in range(5)

][[1e-06, 3.0], [0.001, 3.0], [0.001, 5.0], [1e-06, 5.0], [1.0, 3.0]]

When looking at val_avg for PR-AUC, the first two sets of hyperparameters in the table demonstrate the same performance, hence, we choose the one with larger alpha (=0.001) as it leads to a more conservative model. Because of the way we find the best number of boosting rounds when we use early stopping, one might question whether we use enuogh number of boosting rounds? I decided to run the same grid search as above, this time withough early stopping and also setting the maximum number of boosting rounds to 10000. In addition, we keep track of the variation of logloss and aucpr for the training and validation data with the number of boosting rounds.

tmp_df_no_early, evals = cv_search_params(X_train, y_train, cur_params, all_features, rskf,

eval_metric=['logloss','aucpr'],

num_boost_rounds=10000, early_stop_rounds=None)

tmp_df_no_early.to_pickle(f'hyperparam3_10000.pkl')

with open(f'hyperparam3_10000_evals.pkl', 'wb') as pickle_file:

pickle.dump(evals, pickle_file)

Grid search on:

{'alpha': array([1.e-06, 1.e-03, 1.e+00, 1.e+03]),

'colsample_bylevel': 1,

'colsample_bytree': 1,

'gamma': array([1., 3., 5., 7., 9.]),

'learning_rate': 0.002,

'max_depth': 3,

'min_child_weight': 30,

'scale_pos_weight': 1,

'subsample': 1}

started at 2021-06-09 05:23:46.155894

Total number of hyperparameter candidates = 20

CV 1 on:

{'alpha': 1e-09, 'gamma': 1.0}

started!

Summary:

mean PR-AUC training = 0.815

mean PR-AUC validation = 0.789

mean PR-AUC difference = 0.0258

CV 1 ended! (took 1753.62 seconds)

CV 2 on:

{'alpha': 1e-09, 'gamma': 3.0}

started!

Summary:

mean PR-AUC training = 0.811

mean PR-AUC validation = 0.788

mean PR-AUC difference = 0.0235

CV 2 ended! (took 1659.27 seconds)

CV 3 on:

{'alpha': 1e-09, 'gamma': 5.0}

started!

Summary:

mean PR-AUC training = 0.807

mean PR-AUC validation = 0.785

mean PR-AUC difference = 0.0220

CV 3 ended! (took 1573.70 seconds)

CV 4 on:

{'alpha': 1e-09, 'gamma': 7.0}

started!

Summary:

mean PR-AUC training = 0.805

mean PR-AUC validation = 0.781

mean PR-AUC difference = 0.0236

CV 4 ended! (took 1542.03 seconds)

CV 5 on:

{'alpha': 1e-09, 'gamma': 9.0}

started!

Summary:

mean PR-AUC training = 0.801

mean PR-AUC validation = 0.777

mean PR-AUC difference = 0.0237

CV 5 ended! (took 1503.45 seconds)

CV 6 on:

{'alpha': 1e-06, 'gamma': 1.0}

started!

Summary:

mean PR-AUC training = 0.815

mean PR-AUC validation = 0.789

mean PR-AUC difference = 0.0258

CV 6 ended! (took 1759.45 seconds)

CV 7 on:

{'alpha': 1e-06, 'gamma': 3.0}

started!

Summary:

mean PR-AUC training = 0.811

mean PR-AUC validation = 0.788

mean PR-AUC difference = 0.0235

CV 7 ended! (took 1674.50 seconds)

CV 8 on:

{'alpha': 1e-06, 'gamma': 5.0}

started!

Summary:

mean PR-AUC training = 0.807

mean PR-AUC validation = 0.785

mean PR-AUC difference = 0.0220

CV 8 ended! (took 1590.78 seconds)

CV 9 on:

{'alpha': 1e-06, 'gamma': 7.0}

started!

Summary:

mean PR-AUC training = 0.805

mean PR-AUC validation = 0.781

mean PR-AUC difference = 0.0236

CV 9 ended! (took 1560.62 seconds)

CV 10 on:

{'alpha': 1e-06, 'gamma': 9.0}

started!

Summary:

mean PR-AUC training = 0.801

mean PR-AUC validation = 0.777

mean PR-AUC difference = 0.0237

CV 10 ended! (took 1539.97 seconds)

CV 11 on:

{'alpha': 0.001, 'gamma': 1.0}

started!

Summary:

mean PR-AUC training = 0.815

mean PR-AUC validation = 0.789

mean PR-AUC difference = 0.0257

CV 11 ended! (took 1793.02 seconds)

CV 12 on:

{'alpha': 0.001, 'gamma': 3.0}

started!

Summary:

mean PR-AUC training = 0.811

mean PR-AUC validation = 0.788

mean PR-AUC difference = 0.0234

CV 12 ended! (took 1690.34 seconds)

CV 13 on:

{'alpha': 0.001, 'gamma': 5.0}

started!

Summary:

mean PR-AUC training = 0.807

mean PR-AUC validation = 0.785

mean PR-AUC difference = 0.0221

CV 13 ended! (took 1600.69 seconds)

CV 14 on:

{'alpha': 0.001, 'gamma': 7.0}

started!

Summary:

mean PR-AUC training = 0.805

mean PR-AUC validation = 0.781

mean PR-AUC difference = 0.0236

CV 14 ended! (took 1561.39 seconds)

CV 15 on:

{'alpha': 0.001, 'gamma': 9.0}

started!

Summary:

mean PR-AUC training = 0.801

mean PR-AUC validation = 0.777

mean PR-AUC difference = 0.0237

CV 15 ended! (took 1534.42 seconds)

CV 16 on:

{'alpha': 1.0, 'gamma': 1.0}

started!

Summary:

mean PR-AUC training = 0.813

mean PR-AUC validation = 0.789

mean PR-AUC difference = 0.0247

CV 16 ended! (took 1747.98 seconds)

CV 17 on:

{'alpha': 1.0, 'gamma': 3.0}

started!

Summary:

mean PR-AUC training = 0.809

mean PR-AUC validation = 0.786

mean PR-AUC difference = 0.0230

CV 17 ended! (took 1656.95 seconds)

CV 18 on:

{'alpha': 1.0, 'gamma': 5.0}

started!

Summary:

mean PR-AUC training = 0.806

mean PR-AUC validation = 0.783

mean PR-AUC difference = 0.0225

CV 18 ended! (took 1587.28 seconds)

CV 19 on:

{'alpha': 1.0, 'gamma': 7.0}

started!

Summary:

mean PR-AUC training = 0.803

mean PR-AUC validation = 0.779

mean PR-AUC difference = 0.0241

CV 19 ended! (took 1556.41 seconds)

CV 20 on:

{'alpha': 1.0, 'gamma': 9.0}

started!

Summary:

mean PR-AUC training = 0.800

mean PR-AUC validation = 0.775

mean PR-AUC difference = 0.0244

CV 20 ended! (took 1520.48 seconds)

Grid search ended at 2021-06-09 16:10:16.820294

Variation of logloss and PR-AUC for alpha=0.001 and different values of gamma

fig = plt.figure(dpi=280, figsize=(16,8))

num_folds = 20

test_params = {'alpha': [1e-3], 'gamma':[1., 3., 5., 7., 9.]}

test_evals = evals[10:15]

metrics = ['logloss','aucpr']

num_cases = len(list(product(*test_params.values())))

colors=[plt.cm.terrain(int(i/num_cases*256)) for i,_ in enumerate(product(*test_params.values()))]

step=1000

num_trees=10000

for j,metric in enumerate(metrics):

ax = fig.add_subplot(1,2,j+1)

for i,(alpha,gamma) in enumerate(product(*test_params.values())):

eval_tr = np.mean(np.asarray([test_evals[i][x]['train'][metric] for x in range(num_folds)]), axis=0)[::step]

eval_val = np.mean(np.asarray([test_evals[i][x]['eval'][metric] for x in range(num_folds)]), axis=0)[::step]

len_eval = len(np.mean(np.asarray([test_evals[i][x]['train'][metric] for x in range(num_folds)]), axis=0))

x_data = np.arange(1,len(eval_tr)+1)*step

ax.plot(x_data, eval_tr,

marker='o', markersize=6,

markerFaceColor='white',

color=colors[i],

label=f"alpha={alpha}, gamma={gamma} (tr-{metric})")

ax.plot(x_data, eval_val,

marker='s', markersize=6,

markerFaceColor='white',

color=colors[i], linestyle=':',

label=f"alpha={alpha}, gamma={gamma} (val-{metric})")

ax.set_xlabel('number of boosting rounds', fontsize=18)

ax.set_ylabel(f'{metric}', fontsize=18, labelpad=15)

legend_loc = {0:'upper', 1:'lower'}.get(j)

ax.legend(loc=f"{legend_loc} right",fontsize=12)

plt.suptitle('variation of logloss and PR-AUC with the number of\n' +

'boosting rounds for alpha=0.001 and gamma=[1,3,5,7,9]',

fontsize=22)

plt.show()

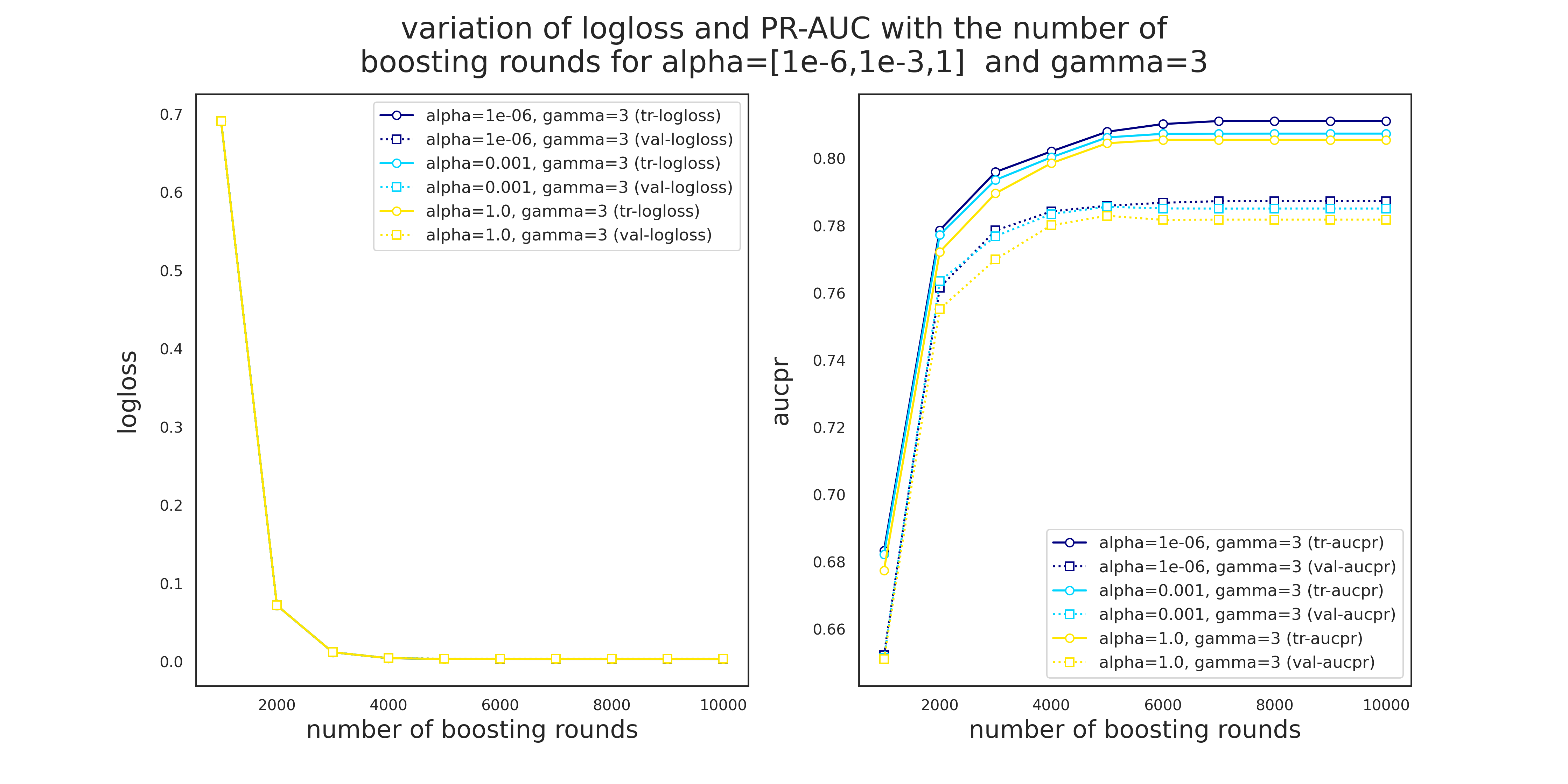

Variation of logloss and PR-AUC for gamma=3 and different values of alpha

fig = plt.figure(dpi=280, figsize=(16,8))

num_folds = 20

test_params = {'alpha': np.logspace(-6,0,3), 'gamma':[3]}

test_evals = [evals[i] for i in [6,7,8]]

metrics = ['logloss','aucpr']

num_cases = len(list(product(*test_params.values())))

colors=[plt.cm.jet(int(i/num_cases*256)) for i,_ in enumerate(product(*test_params.values()))]

step=1000

num_trees=10000

for j,metric in enumerate(metrics):

ax = fig.add_subplot(1,2,j+1)

for i,(alpha,gamma) in enumerate(product(*test_params.values())):

eval_tr = np.mean(np.asarray([test_evals[i][x]['train'][metric] for x in range(num_folds)]), axis=0)[::step]

eval_val = np.mean(np.asarray([test_evals[i][x]['eval'][metric] for x in range(num_folds)]), axis=0)[::step]

len_eval = len(np.mean(np.asarray([test_evals[i][x]['train'][metric] for x in range(num_folds)]), axis=0))

x_data = np.arange(1,len(eval_tr)+1)*step

ax.plot(x_data, eval_tr,

marker='o', markersize=6,

markerFaceColor='white',

color=colors[i],

label=f"alpha={alpha}, gamma={gamma} (tr-{metric})")

ax.plot(x_data, eval_val,

marker='s', markersize=6,

markerFaceColor='white',

color=colors[i], linestyle=':',

label=f"alpha={alpha}, gamma={gamma} (val-{metric})")

ax.set_xlabel('number of boosting rounds', fontsize=18)

ax.set_ylabel(f'{metric}', fontsize=18, labelpad=15)

legend_loc = {0:'upper', 1:'lower'}.get(j)

ax.legend(loc=f"{legend_loc} right",fontsize=12)

plt.suptitle('variation of logloss and PR-AUC with the number of\n' +

'boosting rounds for alpha=[1e-6,1e-3,1] and gamma=3',

fontsize=22)

plt.show()

There are a few observations to make from Figures 4 and 5.

- Unlike Pr-AUC, Logloss is insensitive to the variation of

alphaandgamma. This is most likely due to the severe imbalance of the classes. While PR-AUC is sensitive to imbalance, logloss is about the model's confidence in predicting the correct class, be it positive or negative. - Validation PR-AUC reaches its peak somewhere around 5000 trees followed by a slight reduction and then it plateaus. Train PR-AUC on the other hand is strictly increasing. This causes the gap between the training and validation PR-AUC to increase, i.e., overitting.

- Model is more sensitive to the variation of

gammathanalpha. - 5000 seems to be a safe maximum for the number of boosting rounds.

gamma=3 and alpha=1e-3 to the next round of grid search.

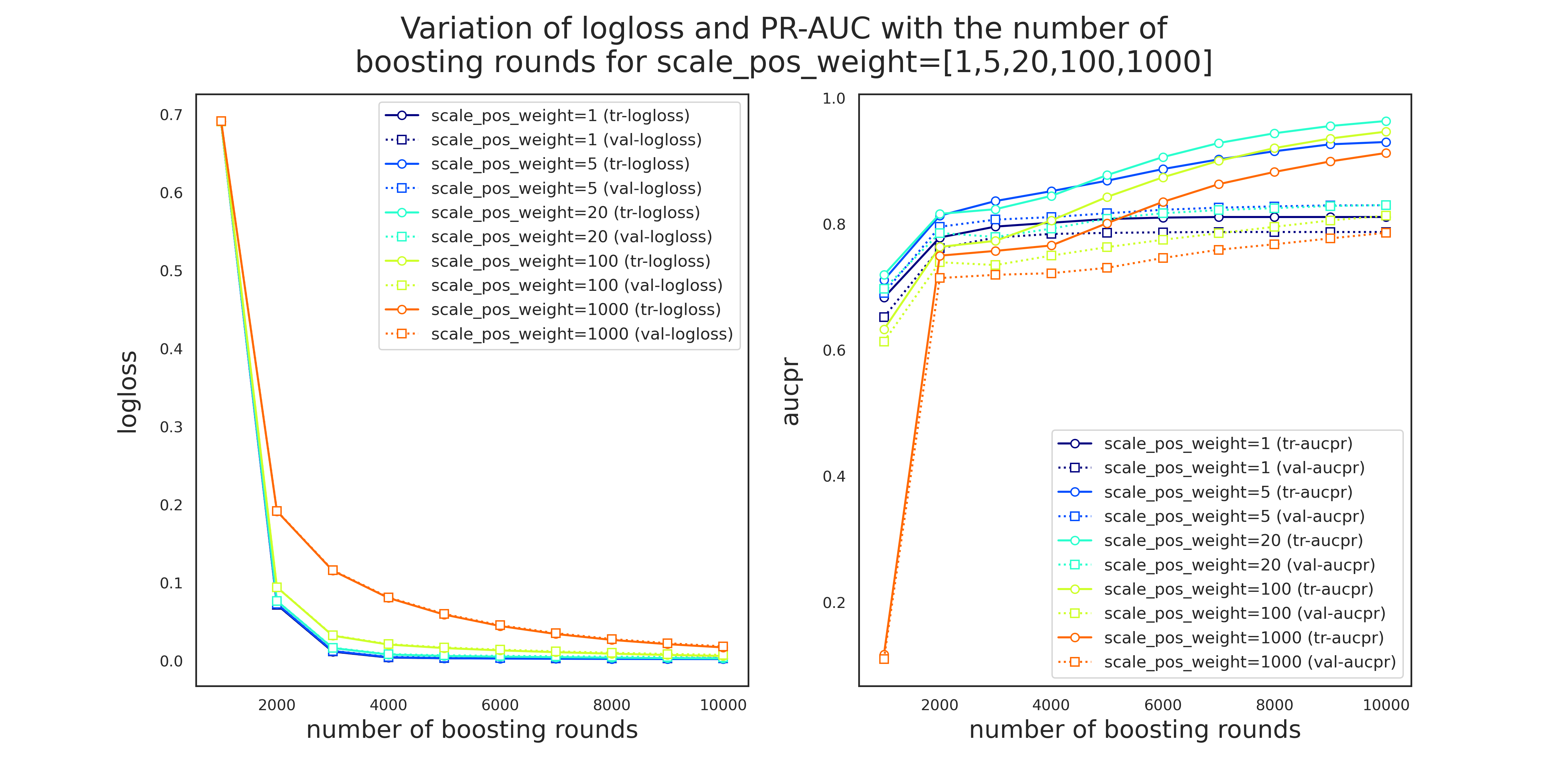

cur_params = tmp_df[tmp_df['diff']<threshold].sort_values('val_avg', ascending=False)['current_params'].iloc[1]Gridsearch for parameter group 4: scale_pos_weight

scale_pos_weight controls the balance of positive and negative weights which is specifically useful when dealing with highly imbalanced cases. A typical value to consider is sum(negative instances)/sum(positive instances), i.e.

from collections import Counter

counter = Counter(df['Class'])

print(f'Class distribution of the response variable: {counter}')

print(f'Majority and minority classes correspond to {100*counter[0]/(counter[0]+counter[1]):.3f}% ',

f'and {100*counter[1]/(counter[0]+counter[1]):.3f}% of the data, respectvively,',

f'\nwith positive-to-negative-ratio = {counter[0]/counter[1]:.1f}')Class distribution of the response variable: Counter({0: 284315, 1: 492})

Majority and minority classes correspond to 99.827% and 0.173% of the data, respectvively,

with positive-to-negative-ratio = 577.9

Therefore, we make sure that this ratio or a value close to it is included in our hyperparameter candidates for scale_pos_weight.

pprint(cur_params){'alpha': 0.001,

'colsample_bylevel': 1,

'colsample_bytree': 1,

'eval_metric': 'aucpr',

'gamma': 3,

'learning_rate': 0.002,

'max_depth': 3,

'min_child_weight': 30,

'objective': 'binary:logistic',

'scale_pos_weight': 1,

'subsample': 1,

'tree_method': 'gpu_hist'}

Note: the only reason to include scale_pos_weight=0.5 in the parameter search is to observe the model behavior.

search_params = param_group_4

cur_params.update(search_params)

pprint(cur_params){'alpha': 0.001,

'colsample_bylevel': 1,

'colsample_bytree': 1,

'gamma': 3,

'learning_rate': 0.002,

'max_depth': 3,

'min_child_weight': 30,

'scale_pos_weight': [0.5, 1, 2, 5, 10, 20, 50, 100, 500 ,1000],

'subsample': 1}

tmp_df, evals = cv_search_params(X_train, y_train, cur_params, all_features, rskf)

tmp_df.to_pickle('hyperparams_round4.pkl') Grid search started at 2021-05-31 14:23:33.726916

Total number of hyperparameter candidates = 10

CV 1 on:

{'scale_pos_weight': 0.5}

started!

Summary:

mean PR-AUC training = 0.729

mean PR-AUC validation = 0.710

mean PR-AUC difference = 0.0191

CV 1 ended! (took 178.08 seconds)

CV 2 on:

{'scale_pos_weight': 1.0}

started!

Summary:

mean PR-AUC training = 0.788

mean PR-AUC validation = 0.772

mean PR-AUC difference = 0.0161

CV 2 ended! (took 260.34 seconds)

CV 3 on:

{'scale_pos_weight': 2.0}

started!

Summary:

mean PR-AUC training = 0.815

mean PR-AUC validation = 0.787

mean PR-AUC difference = 0.0281

CV 3 ended! (took 312.25 seconds)

CV 4 on:

{'scale_pos_weight': 5.0}

started!

Summary:

mean PR-AUC training = 0.829

mean PR-AUC validation = 0.803

mean PR-AUC difference = 0.0281

CV 4 ended! (took 344.57 seconds)

CV 5 on:

{'scale_pos_weight': 10.0}

started!

Summary:

mean PR-AUC training = 0.832

mean PR-AUC validation = 0.801

mean PR-AUC difference = 0.0311

CV 5 ended! (took 299.70 seconds)

CV 6 on:

{'scale_pos_weight': 50.0}

started!

Summary:

mean PR-AUC training = 0.829

mean PR-AUC validation = 0.801

mean PR-AUC difference = 0.0281

CV 6 ended! (took 277.62 seconds)

CV 7 on:

{'scale_pos_weight': 100.0}

started!

Summary:

mean PR-AUC training = 0.762

mean PR-AUC validation = 0.739

mean PR-AUC difference = 0.0241

CV 7 ended! (took 213.36 seconds)

CV 8 on:

{'scale_pos_weight': 500.0}

started!

Summary:

mean PR-AUC training = 0.754

mean PR-AUC validation = 0.731

mean PR-AUC difference = 0.0231

CV 8 ended! (took 195.64 seconds)

CV 9 on:

{'scale_pos_weight': 10000.0}

started!

Summary:

mean PR-AUC training = 0.749

mean PR-AUC validation = 0.715

mean PR-AUC difference = 0.0341

CV 9 ended! (took 190.46 seconds)

CV 10 on:

{'scale_pos_weight': }

started!

Summary:

mean PR-AUC training = 0.759

mean PR-AUC validation = 0.722

mean PR-AUC difference = 0.0361

CV 10 ended! (took 448.14 seconds)

Grid search ended at 2021-05-31 15:21:49.174025

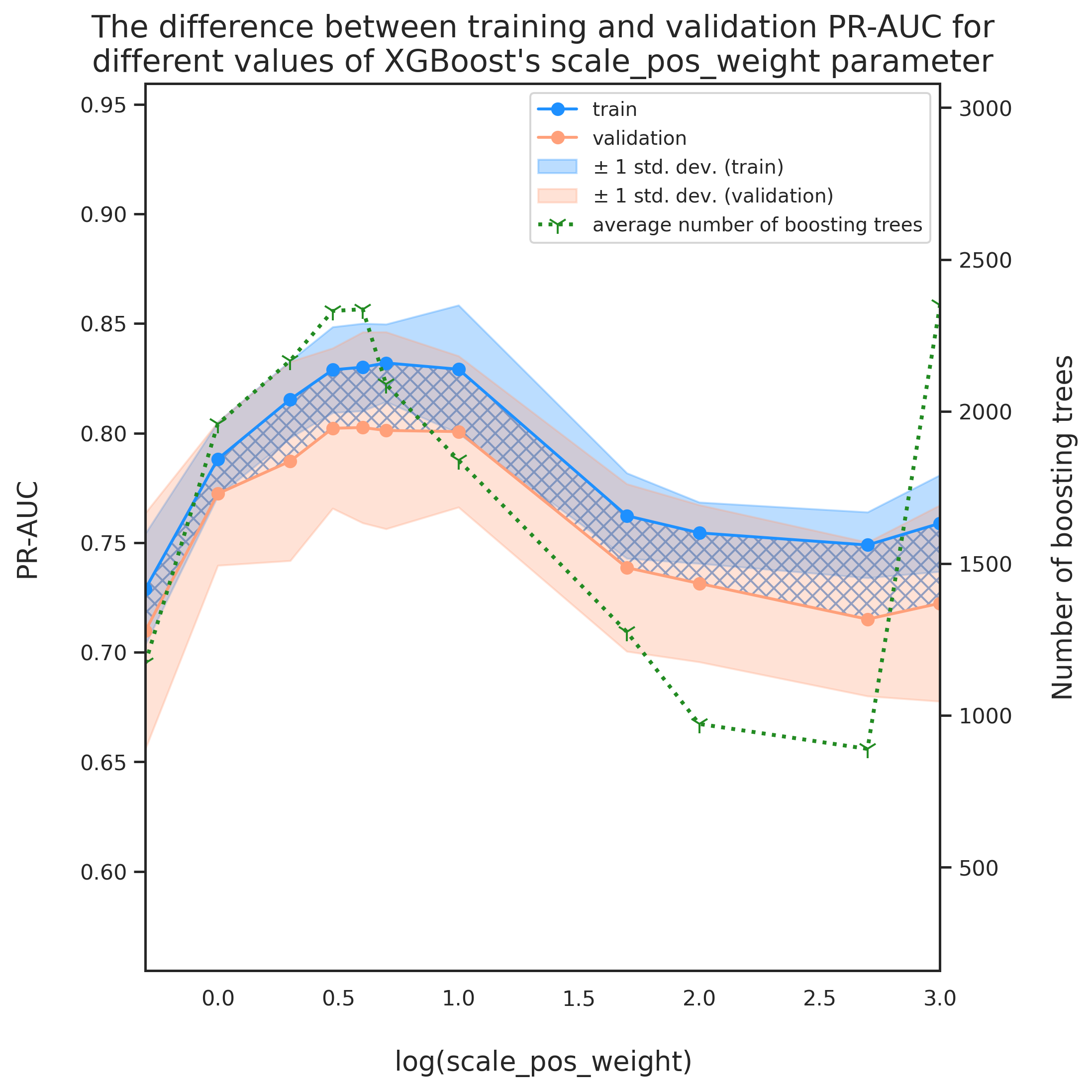

tmp_df[tmp_df['diff']<acceptance_threshold] \

.sort_values('val_avg', ascending=False) \

.head()| current_params | tr_avg | tr_std | val_avg | val_std | numtrees_avg | numtrees_std | diff | time_taken | |

|---|---|---|---|---|---|---|---|---|---|

| 1 | {'max_depth': 3, 'min_child_weight': 30, 'subs... | 0.777 | 0.014 | 0.765 | 0.037 | 307.913 | 301.897 | 0.011 | 0:03:26 |

| 0 | {'max_depth': 3, 'min_child_weight': 30, 'subs... | 0.702 | 0.013 | 0.690 | 0.048 | 91.575 | 169.184 | 0.012 | 0:02:14 |

Note that only two of the search candidates for scale_pos_weight satisfy the acceptance condition.

[x['scale_pos_weight'] for x in tmp_df[tmp_df['diff']<acceptance_threshold] \

['current_params']][0.5, 1]

This is surprising because we expected a value close to sum(negative instances)/sum(positive instances) giving the best model performance. Looking at the variation of evaluation metric with might give us a hint about what might have gone wrong. Plotting the evolution of eval_metric with scale_pos_weight may reveal some more details regarding this discrepancy.

fig = plt.figure(dpi=280, figsize=(8, 8))

ax = fig.add_subplot(111)

labels = []

x_data = [np.log10(x['scale_pos_weight']) for x in tmp_df['current_params']]

colors = ['dodgerblue', 'lightsalmon','forestgreen']

labs = ['train', 'validation']

avgs = ['tr_avg', 'val_avg']

stds = ['tr_std', 'val_std']

stdev_labs = [r'$\pm$ 1 std. dev. (train)', r'$\pm$ 1 std. dev. (validation)']

axes = []

for i, _ in enumerate(avgs):

axes.append(ax.plot(x_data, tmp_df[avgs[i]], marker='o', color=colors[i], label=labs[i]))

for i, _ in enumerate(avgs):

axes.append(ax.fill_between(x_data,

tmp_df[avgs[i]]-tmp_df[stds[i]],

tmp_df[avgs[i]]+tmp_df[stds[i]],

color=colors[i], alpha=.3, label=stdev_labs[i]))

# diff

ax.fill_between(x_data, tmp_df['tr_avg'], tmp_df['val_avg'], color='none',

hatch="XXX", edgecolor="b", linewidth=0.0, alpha=.6)

offset_coef = 0.5

ax.set_xlim([min(x_data), max(x_data)])

ax.set_xlabel('$\log(\mathrm{scale\_pos\_weight})$', fontsize=14, labelpad=20)

ax.set_ylabel('PR-AUC', fontsize=14, labelpad=20)

ax_min = min(min(tmp_df['tr_avg']-tmp_df['tr_std']), min(tmp_df['val_avg']-tmp_df['val_std']))

ax_max = max(max(tmp_df['tr_avg']+tmp_df['tr_std']), max(tmp_df['val_avg']+tmp_df['val_std']))

ax.set_ylim(ax_min-offset_coef*(ax_max-ax_min), ax_max+offset_coef*(ax_max-ax_min))

# plot number of boosting trees

# initiate a second axes that shares the same x-axis

ax2 = ax.twinx()